Link copied!

Theta (Time Decay)

Theta measures the rate at which an option’s value decreases over time, assuming all other factors remain constant. Theta is friendly for option sellers, and it decays faster near the expiration date.

Key Takeaways

- Theta measures how much an option’s value decreases every day as time passes, assuming the price and other factors stay the same. Time decay works against option buyers and favours option sellers, especially as expiry gets closer.

- Time decay is slow when the expiry is far, but it gets faster as the expiry date comes closer. Options lose value quickly near expiry if the price does not move in the buyer’s favour.

- Buyers must get both the price direction and timing right. If the price does not move soon, theta will reduce the option’s value every day, leading to losses.

What is Theta In Options Trading?

Theta is one of the most important Option Greeks, representing the time decay of an options contract. Theta will measure how much the option price will change with time, assuming all other factors (such as stock price, volatility, and interest rates) remain constant.

Theta is negative for both, irrespective of option type, because time decay erodes the value of options as expiration approaches. Time works against the option buyer but favours the option seller.

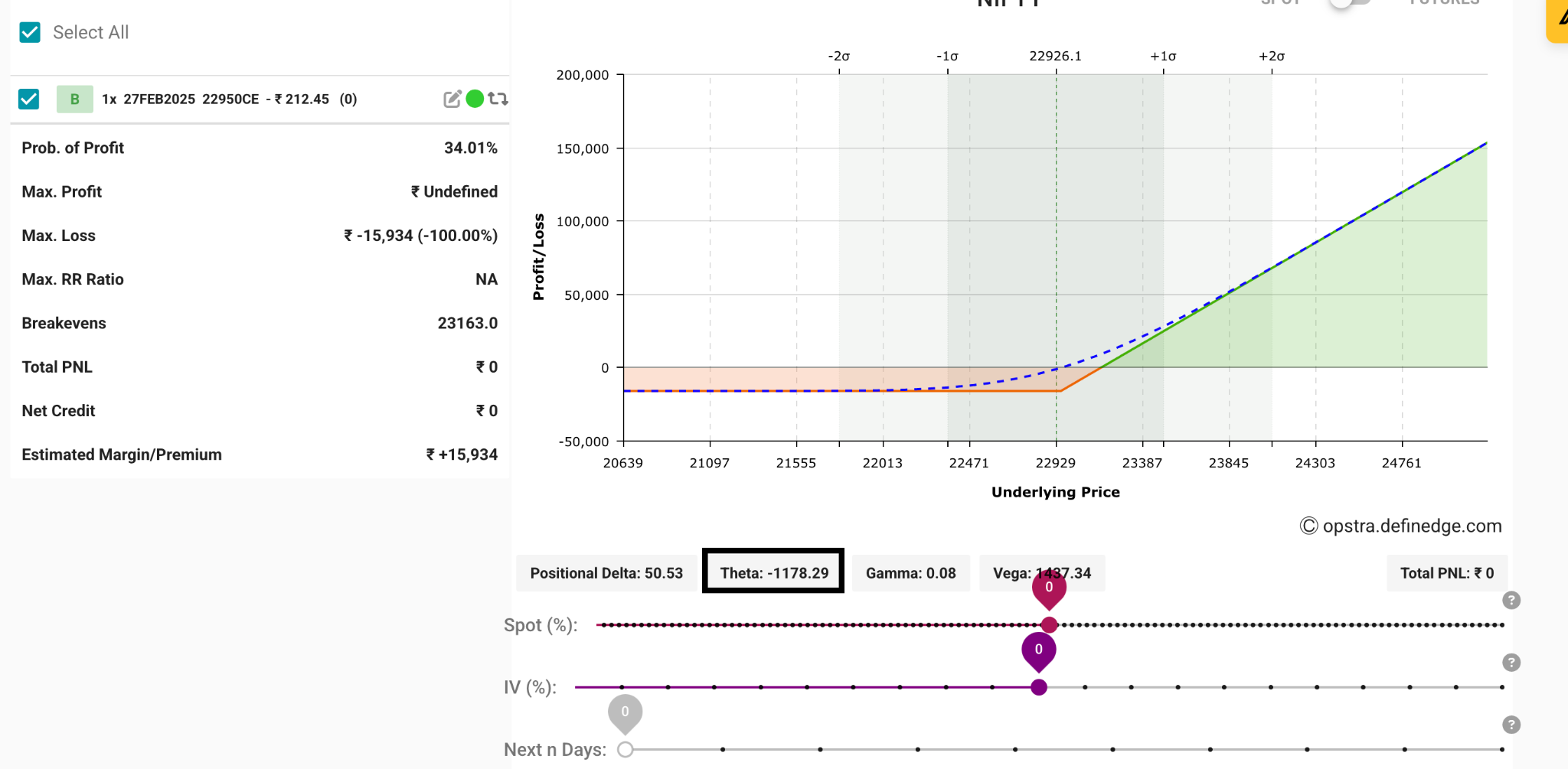

Here is an example of how theta works. The premium of the option contract is Rs 212, and the lot size is 50. So, the total cost of this option is Rs 10,600. The theta is -1178, which means if a buyer holds this option, they will lose Rs 1178 every day from their portfolio because of time decay, assuming everything else remains the same.

How does Theta Decay Work?

Theta measures how much an option loses value with each passing day, assuming all other factors remain constant.

As the expiry date gets closer, the time value of the option gradually decreases. This process is known as theta decay or time decay. If the price of the underlying asset does not move in favour of the option buyer, the option premium keeps reducing every day.

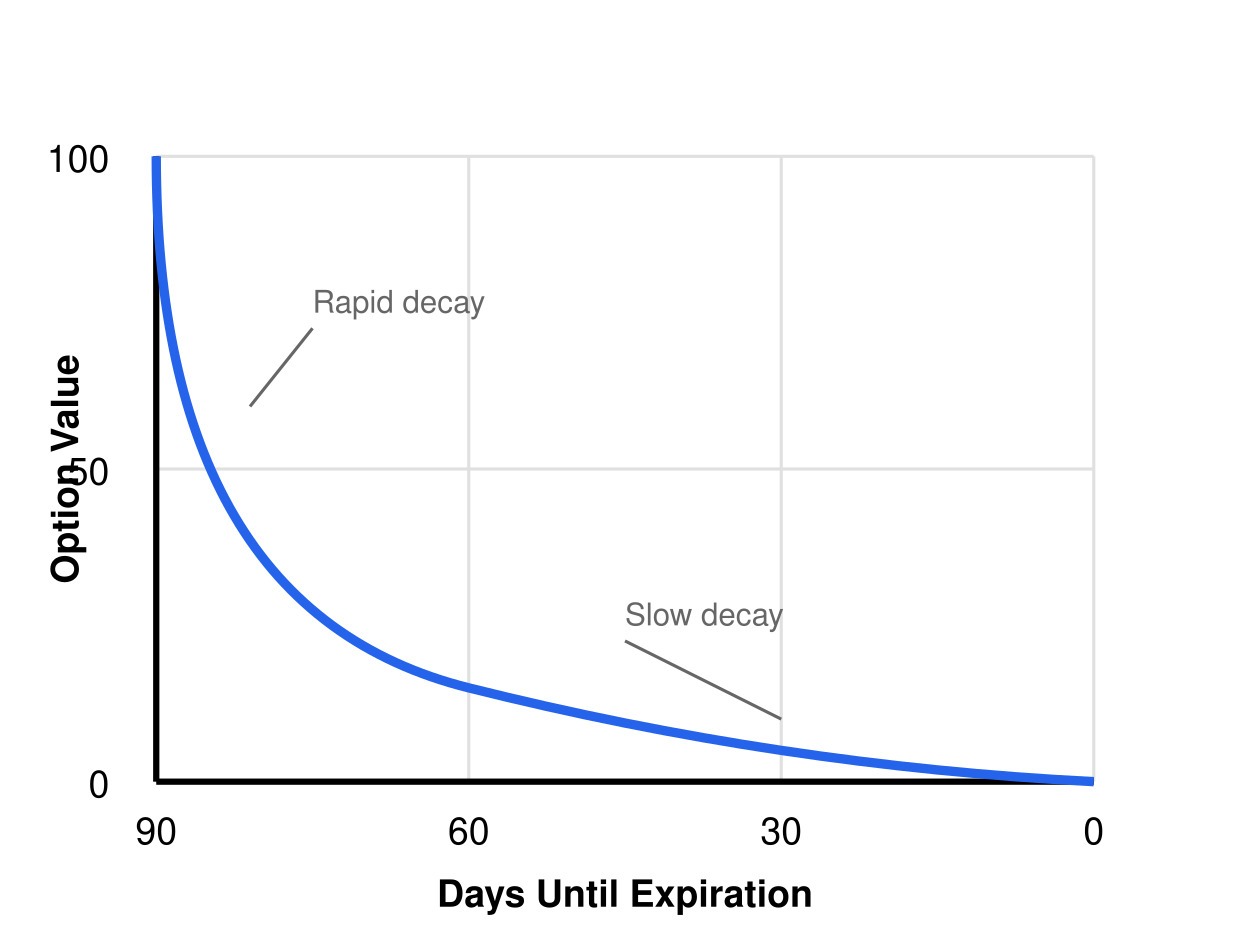

Theta decay is slow when the option has a lot of time left until expiry, but it accelerates rapidly during the final days before expiration.

How to Calculate the Theta Decay?

Theta shows the estimated daily loss in the value of an option because of time decay.

For example, if an option has a theta of -5, the option premium may lose approximately ₹5 every day if all other factors remain unchanged.

Daily Option Value Change = Theta

This calculation helps traders estimate how quickly time decay may reduce the value of their option positions.

Why Does Theta Matter?

Traders cannot ignore theta because it constantly affects their position, even when the market price stays the same.

Time Value Affects the Extrinsic Value Of an Option

Extrinsic value is the additional value stock market participants are willing to pay because of the potential for price movement in the future. More time means more potential for the price to move to a higher extrinsic value. As the expiration date occurs, the time value erodes.

Time Value Affects the Intrinsic Value Of an Option

Theta mainly affects the extrinsic value of an option rather than its intrinsic value.

Intrinsic value represents the actual profit value of the option, while extrinsic value depends on factors like time and volatility.

As time passes, theta reduces the extrinsic value portion of the option premium, eventually causing it to become zero at expiry.

Time Decay Is Not Linear

Time decay does not happen at a constant rate. When an option is far from expiry, time decay moves slowly because there is plenty of time for the price to swing in any direction. However, as the expiry date gets closer, time decay speeds up significantly. Each passing day reduces the option’s value faster because there is less time left for any major price movement to happen.

Here is a pictorial representation showing that theta is not linear. The option premiums become less as they approach the option expiry.

Key Implications for Traders

Understanding how time decay works is only half the picture. What really matters is how it affects your decisions when buying or selling options. Whether you are an option buyer or seller, theta plays a different role in shaping your profits and losses.

Theta Implications For Option Buyers

Option buyers need to consider both the underlying asset direction and the timing right. The underlying has to move in their direction before the theta eats up their value. The more time an option has before expiry, the slower theta works, which gives buyers more room to wait for the price to move. Longer-dated options lose value at a slower pace compared to near-expiry options, making them less affected by theta decay.

Also, read about Option Buying.

Theta Implication For Option Sellers

Theta significantly moves as the near-to-the-expiration option seller to benefit from the time decay they have to sell short-term options. It’s always better to hedge their positions while selling options because they have the potential for unlimited losses.

Theta Risk Factors And Considerations

Knowing how theta affects buyers and sellers helps traders make better choices, but there’s more to it. Theta doesn’t act alone; other factors can change how quickly time decay eats into an option’s value. It’s important to understand these risks and things to watch out for when dealing with theta.

Options Sellers Can Face Significant Losses:

Theta works for option sellers by giving the premium of option contracts. Adverse price movements in the underlying can lead to significant losses.

IV changes can offset Theta decay:

Implied volatility changes the price of an option; the higher the implied volatility, the higher the option price. This can offset the negative effect of theta, which would be a loss for an option seller.

Liquidity Issues in Low-Volume Options:

Low-volume options can be hard to buy or sell quickly when you need to exit. Fewer buyers and sellers often lead to a wide price gap, which can increase your costs. This can reduce profits, especially when theta is already eating into the option’s value.

Time Value and Theta Decay

Time value is directly affected by theta decay.

Options with more time until expiry generally have higher time value because there is a greater possibility of favourable price movement. As expiry approaches, this time value starts declining faster, especially for At-the-Money (ATM) options.

Conclusion

Theta plays a crucial role in options trading as it represents time decay, which gradually reduces an option’s value as expiry approaches. It works against buyers, requiring them to be right about both direction and timing while favouring sellers who profit as time erodes the option’s price. However, traders must understand that theta decay is not linear—it speeds up near expiry.

Sellers also face risks like sharp price movements and volatility spikes, which can offset theta gains. Low liquidity can further complicate exits. A proper understanding of theta, volatility, and risk management helps traders make informed decisions and improve their outcomes.

Frequently Asked Questions (FAQs)

Why is Theta Decay Faster Near Expiry?

Theta decay is not linear. It becomes much faster as the option approaches expiration because there is less time remaining for the underlying asset to move favourably.

Near-expiry options lose value rapidly, especially when the underlying asset price remains stable. This is why option sellers often prefer selling short-term options to benefit from faster theta decay.

What is theta time decay in options?

Theta time decay refers to the gradual reduction in an option’s value as the expiry date approaches. It measures how much premium an option loses daily due to the passage of time.

How to calculate theta time decay in options trading?

Theta time decay is estimated using the theta value of an option contract, which shows the expected daily decline in option premium if market conditions remain unchanged.

For example, if theta is -3, the option premium may decrease by approximately ₹3 per day because of time decay.

What is the impact of theta time decay on option premiums?

Theta decay reduces the extrinsic value of an option premium over time. As expiry approaches, option premiums lose value more rapidly, especially for ATM and OTM options.

This impacts option buyers negatively because the premium keeps decreasing daily, while option sellers may benefit from the reduction in option value.

Is theta good for options?

Theta is good for option sellers because they make money as time decay reduces the option’s value. However, it is bad for option buyers because their option loses value every day if the price doesn’t move as expected.

Why is theta highest at the money?

Theta is highest at the money (ATM) because these options have the most time value. Since the price can move in any direction, the option is more likely to lose value quickly as time passes, making time decay the fastest for ATM options.

Disclaimer: This content is for educational purposes only and does not constitute financial or investment advice. Investments in securities or other financial instruments are subject to market risk, including partial or total loss of capital. Past performance is not indicative of future results. Always consider your financial situation carefully and consult a licensed financial advisor before making investment or trading decisions.

Engineered for the obsessed. Built for traders.

Purpose-built terminals.

Zero compromise.

Built for speed.

Plot No 1290, 2nd Floor, 17th Cross, 5th Main, Sector-7, HSR Layout, Bangalore 560102

Follow us on

Mintcap Brokers Private Limited

CIN – U66110KA2023PTC178706 | Registered Address: Plot No 1290, Second Floor, 17th Cross, 5th Main, Sector-7, HSR Layout, Bangalore 560102 | Tel: 080 – 49552310 | Email ID: compliance@capmint.com | SEBI registered Stock Broker: INZ000322732 | NSE Cash/F&O Member ID: 90430 | BSE Cash/F&O Member ID: 6903 | MCX Member ID: 57400 | NCDEX Member ID: 1312 | SEBI registered Depository Participant: IN-DP-806-2025 | CDSL DP ID: 12102300 | NSE Clearing Member code: M70108 | AMFI-Registered Mutual Fund Distributor: ARN-289109 (Valid upto 28-Feb-2027) | Category II Execution Only Platform : E6903

Details of Client Bank Account

Compliance Officer: Ms. Shridevi Vungarala | Email ID: compliance@capmint.com | Tel no. + 91 9035330126 | Grievance Redressal Officer (GRO) – Ms. Shikha Gupta | Email ID: Grievance@capmint.com | Tel no: 9035331595.

Procedure to file a complaint on SEBI SCORES: Register on SCORES portal. Mandatory details for filing complaints on SCORES: Name, PAN, Address, Mobile Number, E-mail ID. Benefits: Effective Communication, Speedy redressal of the grievances. You may refer the website https://scores.sebi.gov.in/ for more information. You may also download the SEBI Scores app to log a complaint Android: https://play.google.com > store > apps > sebiscores iOS: https://apps.apple.com > app > sebiscores

Disclaimer

Investment in the securities market are subject to market risks, read all the related documents carefully before investing. Brokerage will not exceed the SEBI prescribed limit.

Mutual fund investments are subject to market risks, read all scheme related documents carefully before investing. Mutual Funds are not exchange-traded products.

Attention Investor:

- Stock Brokers can accept securities as margin from clients only by way of pledge in the depository system w.e.f. September 1, 2020.

- Update your mobile number & email Id with your stock broker/depository participant and receive OTP directly from depository on your email id and/or mobile number to create pledge.

- Pay 20% as upfront margin of the transaction value to trade in cash market segment.

- Investors may please refer to the Exchange’s Frequently Asked Questions (FAQs) issued vide circular reference NSE/INSP/45191 dated July 31, 2020 and NSE/INSP/45534 dated August 31, 2020 and other guidelines issued from time to time in this regard.

- Check your Securities /MF/ Bonds in the consolidated account statement issued by NSDL/CDSL every month.