Link copied!

A Daily Margin Statement is a report issued by brokers to traders detailing margin requirements, available balance, utilised margin, and any shortfalls in their trading account for a given trading day. It helps traders track their margin status and ensures compliance with regulatory requirements.

Key Takeaways

- Daily Margin Statement Helps Monitor Trading Funds: It provides details of available, utilised, and required margin, ensuring traders can track their financial position and avoid penalties.

- Understanding Different Types of Margins is Crucial: SPAN Margin covers standard risks, Exposure Margin acts as an extra buffer, and Mark-to-Market (MTM) Margin adjusts for daily price fluctuations.

- Maintaining Sufficient Margin Prevents Risks: A margin shortfall can lead to penalties or forced liquidation of positions, making it essential to keep funds above the required threshold.

- Collateral Haircuts and Market Fluctuations Affect Margin Availability: Pledged securities undergo a haircut, reducing usable margin, while market volatility can suddenly increase margin requirements.

- Regular Review of the Statement Ensures Better Trading Decisions: Misinterpreting margin values or ignoring the report can lead to costly mistakes, making daily checks essential for risk management.

What is the Daily Margin Statement?

A Daily Margin Statement is a report issued by brokers to traders at the end of each trading day, providing a detailed breakdown of their margin status. It includes information on total margin requirements, available funds, utilised margin, shortfalls (if any), and margin excess or deficit. This statement helps traders track their fund utilisation, ensure compliance with regulatory requirements, and manage their risk effectively. It is a crucial tool for monitoring trading positions and avoiding margin calls or potential penalties due to insufficient funds.

Many traders, particularly those new to F&O, tend to overlook this statement in the flurry of daily emails from their broker. This is a mistake. The margin statement is often the earliest indicator that a position is becoming capital-intensive, sometimes a full day before a margin call actually arrives.

Why is Margin Important?

Margin plays a critical role in trading, acting as a safeguard to ensure that traders can meet their financial obligations in the market. Here’s why maintaining margin is essential:

Prevents Forced Liquidation

If a trader doesn’t maintain the required margin, their positions may be forcibly closed by the broker, leading to unexpected losses. This typically happens without prior warning during sharp intraday moves, and the liquidation price is almost always worse than what the trader would have chosen voluntarily.

Reduces Financial Risk

Margin requirements help traders manage risk by ensuring they have adequate funds to cover potential losses from market fluctuations.

Avoids Regulatory Penalties

Market regulators, such as SEBI, impose penalties for margin shortfalls. Keeping an adequate margin helps traders stay compliant and avoid fines. The penalty structure is tiered: shortfalls below ₹1 lakh attract a 0.5% daily penalty, while shortfalls of ₹1 lakh and above attract 1%, and these charges compound quickly if left unaddressed for multiple days.

Enhances Trading Leverage

Traders can take larger positions with margin than with only their cash balance, allowing for greater profit potential, though this also increases risk.

Types of Margins Explained

Understanding different types of margins is crucial for traders, as each serves a distinct purpose in managing financial risk. Let’s break them down in detail:

1. Initial Margin

Before a trader can place an order, they need to deposit a minimum amount called the Initial Margin. This ensures that the trader has sufficient capital to cover potential losses from the trade. The required initial margin varies based on the type of asset and market volatility.

For example, if a trader buys Nifty Futures worth ₹10,00,000, they must pay an Initial Margin, which includes SPAN Margin (₹1,00,000 at 10%) and Exposure Margin (₹20,000 at 2%), totalling ₹1,20,000. This ensures the trader has enough funds to cover potential risks.

2. Maintenance Margin

Once a position is open, traders must maintain a minimum balance in their account, known as the Maintenance Margin. If the margin drops below this threshold due to market fluctuations, a margin call is issued, requiring the trader to add more funds or risk having their position squared off. The time window to meet a margin call varies by broker, but in practice, during sharp intraday declines, some brokers begin auto-squaring off positions within minutes rather than waiting until end of day.

3. SPAN Margin

The SPAN (Standard Portfolio Analysis of Risk) Margin is used for derivative trades and is calculated based on the worst possible price movement of a contract. It acts as the first line of defence in risk management by covering potential losses from extreme market swings. SPAN margin is recalculated multiple times during the trading day, so a position that was comfortably within margin at 10 AM can become margin-deficient by 2 PM if volatility spikes.

4. Exposure Margin

While SPAN Margin accounts for standard risks, Exposure Margin is an additional buffer collected by brokers to safeguard against unexpected market volatility. It is usually a fixed percentage of the trade value and applies to futures and short options positions in the derivatives segment.

5. Mark-to-Market (MTM) Margin

The Mark-to-Market (MTM) Margin represents daily gains or losses on open positions. If a trader incurs a loss at the end of the trading day, they must deposit additional funds to cover the shortfall. Conversely, if they make a profit, the gains are credited to their account. MTM settlements happen on a T+1 basis, meaning the debit or credit appears in the trading account the next morning. Traders who carry overnight futures positions should account for this daily cash flow when planning their margin buffer.

6. Delivery Margin

When a trader chooses to hold stocks until delivery settlement, a Delivery Margin is levied. This ensures that they have enough funds to complete the transaction, reducing counterparty risks.

7. Additional/Ad-hoc Margins

Brokers may impose Additional or Ad-hoc Margins in certain situations, such as periods of high volatility or unexpected market events. These margins help maintain stability and ensure adequate risk coverage for open positions. During events like union budget announcements or sudden geopolitical escalations, ad-hoc margins of 2–5% have been imposed on select stocks with little advance notice, catching under-margined traders off guard.

By understanding these margin types, traders can make informed financial decisions, avoid unnecessary penalties, and optimise their trading strategies effectively.

Key Components of a Daily Margin Statement

A Daily Margin Statement provides a comprehensive summary of a trader’s margin position. It includes several key components that help traders monitor their available funds, margin utilisation, and compliance with regulatory requirements.

Funds (Cash Balance)

This shows the total cash available in the trader’s account for trading. It can be used to fulfil margin requirements.

Value of Securities (After Haircut)

This is the value of pledged securities after a haircut is applied. A haircut is a percentage deduction made by the exchange to account for price changes and risks. Haircuts on pledged equity collateral typically range from 10% to 50% depending on the stock’s liquidity and volatility category, so a ₹1 lakh holding may only contribute ₹50,000 to ₹90,000 in usable margin.

Any Other Approved Margin

This includes additional sources of margin, such as Fixed Deposits (FDs), bank guarantees, or other collateral that the exchange has approved. These can also help meet margin obligations.

Upfront Margin Required

This is the minimum margin needed to start new trades. It is calculated based on exchange rules and risk parameters, including SPAN and Exposure Margins.

Consolidated Crystallised Obligation (CCO)

This represents the net obligations from settled or closed-out positions, including realised losses, delivery obligations, and other charges that need to be funded from the trading account.

Total Margin Required (End of Day)

This is the final margin needed to maintain all open positions. It includes SPAN Margin, Exposure Margin, and Mark-to-Market (MTM) adjustments based on daily price changes.

Margin Utilised/Collected

This shows the part of the available margin that has already been used for keeping open trades. It indicates the trader’s remaining margin balance.

Excess or Shortfall

If the trader’s available margin is greater than the required margin, it is called an excess margin, which allows for extra trades. If there is a shortfall, the trader will need to add funds to avoid penalties or having their positions liquidated. Even a small shortfall of ₹500–1,000 can trigger a penalty entry, so rounding up your available margin rather than running it exactly to the requirement is a practical habit.

Penalty (if any)

If the margin goes below regulatory requirements, the exchange or broker may impose a penalty, which could result in additional financial consequences.

This statement helps traders track their margin status, prevent margin calls, and ensure smooth trading operations while complying with SEBI and exchange regulations.

How to Read a Daily Margin Statement

A Daily Margin Statement provides traders with crucial insights into their margin status, helping them track available funds, utilised margin, and any shortfalls. Properly interpreting this statement can help traders avoid penalties, manage risks effectively, and optimise fund utilisation.

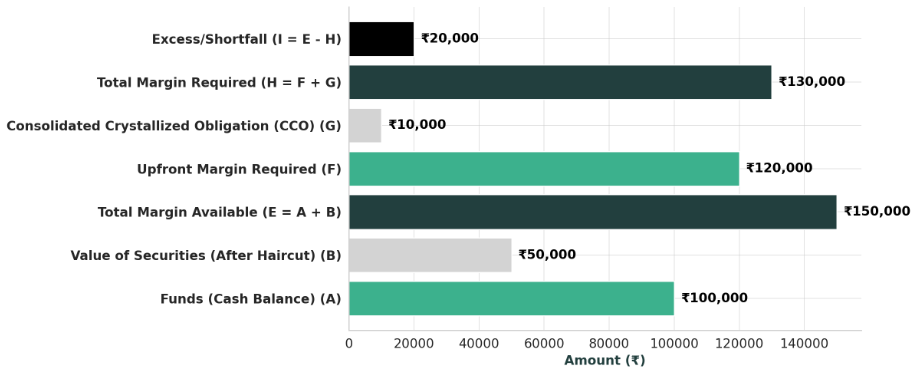

Let’s try to understand how to interpret a daily margin statement with an example. Consider an investor, Mr Anil, who has the following details in his daily margin statement:

| Component | Amount (₹) | Explanation |

|---|---|---|

| Funds (A) | ₹1,00,000 | Cash available in the trading account. |

| Value of Securities After Haircut (B) | ₹50,000 | Pledged securities after haircut deductions. |

| Total Margin Available (E = A + B) | ₹1,50,000 | The total margin that can be used for trading. |

| Total Upfront Margin Required (F) | ₹1,20,000 | The margin required for open positions. |

| Consolidated Crystallised Obligation (G) | ₹10,000 | Additional obligations, such as fees and MTM losses. |

| Total Margin Required (H = F + G) | ₹1,30,000 | The total amount required to avoid a shortfall. |

| Excess/Shortfall (I = E − H) | ₹20,000 (Excess) | Extra funds available for new positions. |

What Does This Mean for Mr Anil?

Mr Anil has a ₹20,000 excess margin, meaning he can take new positions within that margin without incurring penalties. If his available margin falls below ₹1,30,000, he may need to add funds to avoid a margin shortfall.

One detail worth noting: if ₹50,000 of his available margin comes from pledged securities, and those securities drop in value by even 10% overnight, his effective margin available would shrink by approximately ₹5,000, cutting his excess nearly in half. This is why relying heavily on collateral margin without a cash cushion can be deceptive.

SEBI Regulations Related to Daily Margin Statement

- SEBI mandates brokers to send daily margin statements to clients.

- Since September 2020, upfront margin collection is mandatory in the cash segment.

- Any margin shortfall results in penalties, typically passed on to traders.

The upfront margin rule in the cash segment was a significant shift when it was introduced. Prior to this, traders could buy and sell stocks intraday without setting aside any margin, which encouraged excessive leveraged positions. The phased implementation between 2020 and 2021 gradually increased the required upfront percentage from 25% to 100%, and its impact on intraday volumes was noticeable across the industry.

How Can Traders Use Daily Margin Statements Efficiently?

Maintain a Cushion

Always keep an extra margin to manage market fluctuations and avoid penalties. A buffer of 15–20% above the total required margin provides a reasonable safety net against intraday SPAN recalculations and overnight MTM debits.

Monitor Pledged Securities

Keep track of haircut adjustments to ensure the collateral value remains sufficient. Haircut percentages can change if the exchange reclassifies a stock into a higher volatility group, which sometimes happens without prominent advance notice.

Use Pledged Shares Wisely

If using pledged shares as margin, track their value daily to prevent unexpected margin shortfalls. For example, Priya pledges ₹5 lakhs worth of stocks and gets ₹4 lakhs in margin. She trades requiring ₹3.5 lakhs, but if her pledged stock value drops, her margin availability reduces, increasing risk.

Be Aware of Peak Margin Requirements

Intraday trading impacts margin obligations, so ensure compliance with peak margin norms. The exchange takes four random snapshots of positions during the day to calculate peak margin, and any shortfall at any of these snapshots can trigger a penalty, not just the end-of-day position.

Optimise Margin Utilisation Strategically

Efficiently manage cash and collateral to make the most of available margin while reducing unnecessary risks. One practical approach is to maintain at least 50% of total margin in cash rather than relying entirely on pledged collateral, since cash margin doesn’t fluctuate with market movements.

By following these practices, traders can efficiently manage their margin, stay compliant with regulations, and ensure seamless trading operations.

Real-Life Example

Priya, a trader, pledges stocks worth ₹5 lakhs and gets ₹4 lakhs in margin after a haircut. She keeps ₹10,000 in cash, making her total margin ₹4.1 lakhs. She takes a position requiring ₹3.5 lakhs, leaving an excess of ₹60,000.

The next day, if her stock value falls by ₹50,000, her margin available drops to ₹3.6 lakhs. Now, she has only ₹10,000 excess margin. If the stock falls further, she may face a margin shortfall and penalties.

What makes this situation particularly tricky is that the pledged stocks and the traded position can move against Priya simultaneously. If she has pledged IT sector stocks and is also holding IT futures, a broad sectoral decline erodes both her collateral value and her position margin at the same time. This correlated risk is something that the margin statement captures clearly, but only if Priya reviews it daily rather than waiting for a margin call alert.

Conclusion

A Daily Margin Statement is crucial for traders to monitor their funds, comply with regulations, and manage risk effectively. Understanding its components helps traders make informed decisions and avoid penalties. Making it a habit to review the statement each evening, even briefly, takes only a few minutes but can prevent costly surprises the following morning.

Frequently Asked Questions (FAQs)

What is a daily margin statement on the NSE?

It’s a report from your broker showing how much margin you have, how much is used, and how much is needed to keep your trades open.

Why is the daily margin statement important?

It helps you track your funds, avoid penalties, and stay within SEBI rules. Checking it daily can prevent unexpected issues, particularly when carrying overnight derivative positions where SPAN margin can shift between sessions.

Who gets this statement?

All traders using margin get this statement from their broker at the end of each trading day.

What does “margin required” mean?

It’s the total amount you need to keep your trades open, including different types of margins like SPAN and Exposure. This figure can change from day to day based on market volatility and any new positions taken.

What happens if I don’t have enough margin?

If your margin is short, you might get a penalty or your broker may sell some of your holdings to cover the shortfall. The penalty is calculated on the shortfall amount and is deducted from the trading account, typically reflected in the next day’s statement.

Does it include brokerage charges?

No, brokerage fees are separate and appear in your trade confirmation or contract note, not in the margin statement.

Disclaimer: This content is for educational purposes only and does not constitute financial or investment advice. Investments in securities or other financial instruments are subject to market risk, including partial or total loss of capital. Past performance is not indicative of future results. Always consider your financial situation carefully and consult a licensed financial advisor before making investment or trading decisions.

Engineered for the obsessed. Built for traders.

Purpose-built terminals.

Zero compromise.

Built for speed.

Plot No 1290, 2nd Floor, 17th Cross, 5th Main, Sector-7, HSR Layout, Bangalore 560102

Follow us on

Mintcap Brokers Private Limited

CIN – U66110KA2023PTC178706 | Registered Address: Plot No 1290, Second Floor, 17th Cross, 5th Main, Sector-7, HSR Layout, Bangalore 560102 | Tel: 080 – 49552310 | Email ID: compliance@capmint.com | SEBI registered Stock Broker: INZ000322732 | NSE Cash/F&O Member ID: 90430 | BSE Cash/F&O Member ID: 6903 | MCX Member ID: 57400 | NCDEX Member ID: 1312 | SEBI registered Depository Participant: IN-DP-806-2025 | CDSL DP ID: 12102300 | NSE Clearing Member code: M70108 | AMFI-Registered Mutual Fund Distributor: ARN-289109 (Valid upto 28-Feb-2027) | Category II Execution Only Platform : E6903

Details of Client Bank Account

Compliance Officer: Ms. Shridevi Vungarala | Email ID: compliance@capmint.com | Tel no. + 91 9035330126 | Grievance Redressal Officer (GRO) – Ms. Shikha Gupta | Email ID: Grievance@capmint.com | Tel no: 9035331595.

Procedure to file a complaint on SEBI SCORES: Register on SCORES portal. Mandatory details for filing complaints on SCORES: Name, PAN, Address, Mobile Number, E-mail ID. Benefits: Effective Communication, Speedy redressal of the grievances. You may refer the website https://scores.sebi.gov.in/ for more information. You may also download the SEBI Scores app to log a complaint Android: https://play.google.com > store > apps > sebiscores iOS: https://apps.apple.com > app > sebiscores

Disclaimer

Investment in the securities market are subject to market risks, read all the related documents carefully before investing. Brokerage will not exceed the SEBI prescribed limit.

Mutual fund investments are subject to market risks, read all scheme related documents carefully before investing. Mutual Funds are not exchange-traded products.

Attention Investor:

- Stock Brokers can accept securities as margin from clients only by way of pledge in the depository system w.e.f. September 1, 2020.

- Update your mobile number & email Id with your stock broker/depository participant and receive OTP directly from depository on your email id and/or mobile number to create pledge.

- Pay 20% as upfront margin of the transaction value to trade in cash market segment.

- Investors may please refer to the Exchange’s Frequently Asked Questions (FAQs) issued vide circular reference NSE/INSP/45191 dated July 31, 2020 and NSE/INSP/45534 dated August 31, 2020 and other guidelines issued from time to time in this regard.

- Check your Securities /MF/ Bonds in the consolidated account statement issued by NSDL/CDSL every month.