Table of Content

- Call vs Put Options: Quick Comparison

- What Are Options in the Stock Market?

- Types of Options

- What Is a Call Option?

- What Is a Put Option?

- How to Calculate Call and Put Option Payoffs

- Important Terms Related to Call and Put Options

- When Should You Use a Call and Put Option?

- Common Beginner Mistakes with Options

- Conclusion

- Frequently Asked Questions (FAQs)

Link copied!

Put Option vs. Call Option: A Quick Guide for Beginners

When you are new to the stock market, and someone says that they have bought or sold call options or bought or sold put options, it can get a little confusing at first. But the moment you get the difference between the two, it starts making sense quickly.

Call vs Put Options: Quick Comparison

Before diving into the details, here’s a side-by-side summary for quick reference. You can use this as a cheat sheet and explore the detailed sections below for a deeper understanding of each.

|

Basis |

Call Option |

Put Option |

|---|---|---|

|

Right |

Gives the right to buy a stock at a predetermined price within a set time. You can lock in a lower price today and benefit if the stock rises. |

Gives the right to sell a stock at a predetermined price within a set time. You can secure a higher selling price even if the stock falls. |

|

Market View |

Used when you are bullish, expecting the stock price to rise. A way to profit from upward movements without owning the stock outright. |

Used when you are bearish, expecting the stock price to fall. Lets you benefit from a declining market or protect existing holdings. |

|

Buyer Profits When |

The stock price goes above the strike price plus the premium paid. The higher the price, the more the profit potential. |

The stock price goes below the strike price minus the premium paid. The lower the price, the more the profit. |

|

Seller Profits When |

The stock price stays the same or falls, because the buyer won’t exercise the option, allowing the seller to keep the premium. |

The stock price stays the same or rises, because the buyer won’t exercise the option, letting the seller pocket the premium. |

|

Maximum Loss (Buyer) |

Limited to the premium paid. |

Limited to the premium paid. |

|

Maximum Loss (Seller) |

Theoretically unlimited (stock can rise indefinitely). |

Significant (stock can fall to zero). |

|

Example |

Buying a Reliance Call Option when you expect its price to rise. |

Buying an Infosys Put Option when you expect its price to fall. |

One important distinction that beginners often miss: the buyer and seller of an option have fundamentally different risk profiles. The buyer pays a fixed premium and has limited risk (maximum loss = premium) with potentially large upside. The seller receives the premium upfront but takes on significantly larger risk, because if the trade moves against them, their losses can be substantial. This asymmetry is why option buying is generally more suitable for beginners, while option selling requires a deeper understanding of risk management and usually more capital.

Now, let’s build up from the basics to understand how each of these works in practice.

What Are Options in the Stock Market?

An option is basically a contract that gives you the right, but not the obligation, to buy or sell a stock (or any other asset) at a fixed price within a certain time period. It’s actually quite simple once you think of it like this: imagine booking a movie ticket. You’ve reserved your seat and locked in the price, but you’re not forced to go. If you skip the movie, you just lose the small booking fee, and that’s the premium in trading terms.

Now, in the stock market, options come in two main types: Call Options and Put Options. These are what traders commonly refer to as “calls and puts.” Both give you opportunities to profit from price movements, but they work in opposite directions; one benefits when prices rise, and the other when prices fall.

On Indian exchanges, options are available on the Nifty 50 index, Bank Nifty index, and approximately 180–200 individual stocks in the F&O segment. Nifty and Bank Nifty options account for the overwhelming majority of daily options volume, with weekly expiries on Thursday attracting particularly heavy activity. For beginners, understanding calls and puts using Nifty examples is the most practical starting point because the liquidity is deep and the bid-ask spreads are tight, meaning the cost of learning through small positions is lower than on less liquid stock options.

Types of Options

Additionally, options can be classified based on their relationship with the underlying stock price:

In the Money (ITM)

The option has intrinsic value. For calls, the stock price is greater than the strike price; for puts, the stock price is less than the strike price.

At the Money (ATM)

The stock price is roughly equal to the strike price. Both calls and puts have no intrinsic profit but have time value.

Out of the Money (OTM)

The option currently has no intrinsic value. For calls, the stock price is less than the strike price; for puts, the stock price is greater than the strike price.

Understanding moneyness is one of the first practical skills a beginner needs, because it directly determines how an option is priced and how it behaves as the underlying moves. An ITM option costs more but has a higher probability of finishing profitable. An OTM option is cheaper but needs a larger move in the underlying to become profitable. Many beginners gravitate toward OTM options because the premiums are low, sometimes ₹5–10 per lot, but these options expire worthless far more often than they pay off.

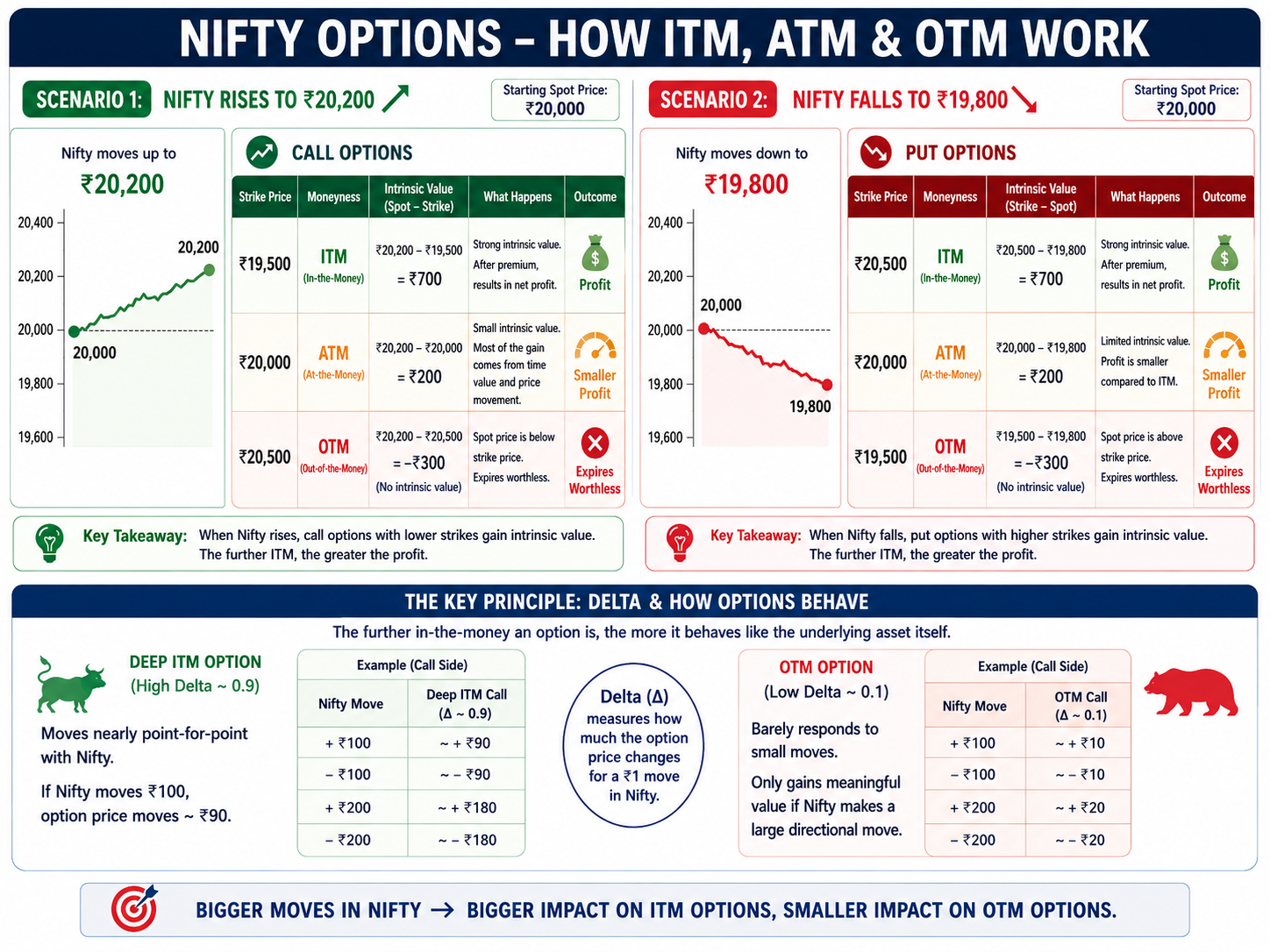

Example with Nifty

Suppose Nifty is at ₹20,000.

Scenario 1: Nifty rises to ₹20,200

- A call option with a strike of ₹19,500 is In-the-Money (ITM). Intrinsic Value = Spot Price − Strike Price = ₹20,200 − ₹19,500 = ₹700 After adjusting for the premium paid, this results in a net profit.

- A call option with a strike of ₹20,000 is At-the-Money (ATM). The intrinsic value is smaller, and most of the gain comes from time value rather than price movement.

- A call option with a strike of ₹20,500 is Out-of-the-Money (OTM). Since the spot price is below the strike price, the option expires worthless.

Scenario 2: Nifty falls to ₹19,800

- A put option with a strike of ₹20,500 is In-the-Money (ITM). Intrinsic Value = Strike Price − Spot Price = ₹20,500 − ₹19,800 = ₹700 After accounting for the premium, this results in a net profit.

- A put option with a strike of ₹20,000 is At-the-Money (ATM). The profit is smaller compared to ITM, as it has limited intrinsic value.

- A put option with a strike of ₹19,500 is Out-of-the-Money (OTM). Since the spot price is above the strike price, the option expires worthless.

These scenarios illustrate a key principle: the further in-the-money an option is, the more it behaves like the underlying asset itself. A deep ITM Nifty call with a delta of 0.9 moves nearly point-for-point with Nifty, while an OTM option with a delta of 0.1 barely responds to small moves and only gains meaningful value if Nifty makes a large directional move.

What Is a Call Option?

A call option is a type of contract that gives you the right to buy a stock at a fixed price (called the strike price) within a specific time period.

Think of it like this: when you believe a stock’s price is going to rise, instead of buying the stock outright, you can buy a call option. This lets you lock in today’s price and benefit later if the price actually goes up. The advantage over buying the stock directly is leverage: a call option lets you participate in the stock’s upside by paying only a fraction of the stock’s price as premium, rather than the full share price.

Example of a Call Option

Scenario 1: Reliance rises to ₹2,600

Let’s say Reliance is trading at ₹2,500. You buy a call option with a strike price of ₹2,500 by paying a premium of ₹50.

Since the stock rises to ₹2,600, the intrinsic value becomes: Intrinsic Value = Spot Price − Strike Price = ₹2,600 − ₹2,500 = ₹100

After adjusting for the premium paid: Net Profit = Intrinsic Value − Premium = ₹100 − ₹50 = ₹50 per share

This results in a 100% return on the premium paid, as you invested ₹50 and earned ₹50. Had you bought Reliance shares directly at ₹2,500, the same ₹100 gain would represent a 4% return on your investment. This difference in percentage returns is the leverage that options provide, though it works equally powerfully in the opposite direction when the trade goes wrong.

Scenario 2: Reliance stays at ₹2,500 or below

If the stock does not move above the strike price, the option has no intrinsic value and expires worthless. Maximum Loss = Premium Paid = ₹50 per share

Your loss is limited only to the premium, and you are not obligated to buy the stock. This defined maximum loss is one of the key advantages of buying options versus buying the stock itself, where the potential loss on a ₹2,500 stock is theoretically the full ₹2,500 if the company goes to zero.

That’s how a call option works; it lets you participate in the upside potential of a stock without actually owning it.

Call = Right to Buy (Bullish View). You buy a call when you expect prices to go up.

What Is a Put Option?

A put option is a type of contract that gives you the right to sell a stock at a fixed price (called the strike price) within a specific time period.

Think of it like this: when you believe a stock’s price is going to fall, instead of short-selling the stock directly, you can buy a put option. This allows you to lock in today’s higher price and benefit later if the stock price actually goes down. Unlike short selling, where losses are theoretically unlimited if the stock keeps rising, buying a put limits your maximum loss to the premium paid.

Example of a Put Option

Scenario 1: Infosys falls to ₹1,400

Let’s say Infosys is trading at ₹1,500. You buy a put option with a strike price of ₹1,500 by paying a premium of ₹40.

Since the stock falls to ₹1,400, the intrinsic value becomes: Intrinsic Value = Strike Price − Spot Price = ₹1,500 − ₹1,400 = ₹100

After adjusting for the premium paid: Net Profit = Intrinsic Value − Premium = ₹100 − ₹40 = ₹60 per share

This gives a 150% return on the ₹40 premium, illustrating the leverage advantage of options when the directional view is correct.

Scenario 2: Infosys stays above ₹1,500

If the stock price does not fall below the strike price, the option has no intrinsic value and expires worthless. Maximum Loss = Premium Paid = ₹40 per share

Your loss is limited to the premium, and you are not obligated to sell the stock.

That’s how a put option works; it allows you to profit from falling stock prices or even hedge your existing positions against downside risk. Put options are also widely used as portfolio insurance: if you hold Infosys shares and are worried about a near-term decline, buying a put effectively puts a floor under your potential losses without requiring you to sell the shares.

Put = Right to Sell (Bearish View). You buy a put when you expect prices to go down.

How to Calculate Call and Put Option Payoffs

|

Option Type |

Position |

Payoff Formula |

Maximum Profit |

Maximum Loss |

|---|---|---|---|---|

|

Call Option |

Long Call (Buyer) |

max(0, Spot Price − Strike Price) − Premium |

Unlimited |

Limited to the premium paid |

|

Call Option |

Short Call (Seller) |

min(0, Strike Price − Spot Price) + Premium |

Limited to the premium received |

Unlimited |

|

Put Option |

Long Put (Buyer) |

max(0, Strike Price − Spot Price) − Premium |

Limited (as price cannot fall below zero) |

Limited to the premium paid |

|

Put Option |

Short Put (Seller) |

min(0, Spot Price − Strike Price) + Premium |

Limited to the premium received |

Significant if the stock price falls sharply |

These formulas describe the payoff at expiry. During the life of the option, the actual profit or loss also depends on time value and implied volatility, which means you can profit or lose money on an option position well before expiry by selling the option at a higher or lower premium than you paid for it. Most active option traders on Indian exchanges close their positions before expiry rather than holding to expiration, particularly on weekly Nifty and Bank Nifty options where time decay accelerates sharply in the final two days.

A practical point for beginners: calculating the breakeven point before entering any option trade is a useful discipline. For a long call, breakeven = strike price + premium. For a long put, breakeven = strike price − premium. If the breakeven requires a move that seems unrealistic given the stock’s typical range over the time remaining to expiry, the trade may not offer favourable odds regardless of how strong your directional conviction is.

Important Terms Related to Call and Put Options

Understanding options also means getting familiar with a few key terms that impact pricing and risk. Let’s break them down:

Intrinsic Value

This is the difference between the underlying stock’s price and the strike price. Only options that are “in-the-money” have intrinsic value. If an option is “out-of-the-money” or “at-the-money,” its intrinsic value is zero. Think of it as the real, immediate value of the option if you exercised it right now. For a Nifty 22,000 call when Nifty is at 22,300, the intrinsic value is ₹300. For a Nifty 22,500 call with Nifty at the same 22,300, the intrinsic value is zero because exercising the option would mean buying at ₹22,500 what you can get in the market for ₹22,300.

Time Value

This is the extra amount you pay over the intrinsic value for the possibility that the stock could move further in your favour before the option expires. It reflects the potential future gains, market expectations, and remaining time. An ATM Nifty option with 30 days to expiry will have significantly more time value than the same option with 2 days to expiry, because there is more time for a favourable move to occur. Time value is what makes options more expensive than their intrinsic value alone, and it’s also what erodes daily as expiry approaches.

Premium

The premium is the upfront cost of buying an option. It’s calculated as:

Premium = Intrinsic Value + Time Value

Even if the trade doesn’t go your way, the maximum loss you face as a buyer is limited to this premium, which makes option buying a controlled-risk proposition. For sellers, the premium received is their maximum profit, which they keep in full only if the option expires worthless.

Theta

Theta measures the rate at which an option loses value as it gets closer to expiration. A higher theta means the option’s value erodes faster over time. Theta works against option buyers (you lose a little value every day just by holding the option) and in favour of option sellers (they benefit from the daily erosion of the premium they received). On weekly Nifty options, theta decay accelerates dramatically in the final two days before Thursday expiry, which is why holding OTM options into the last day or two is statistically unfavourable for buyers.

Time/Theta Decay

Time decay refers to the natural reduction in an option’s value as the expiration date approaches. Options lose value over time even if the stock doesn’t move, which is why timing is critical when trading options. A common beginner mistake is buying an option with a correct directional view but insufficient time for the move to materialise. Buying a weekly option on Monday that requires a 3% move by Thursday is a very different proposition from buying a monthly option that gives the same 3% move four weeks to develop. The weekly option is cheaper in absolute terms but requires the move to happen almost immediately, which dramatically reduces the probability of success.

Implied Volatility (IV)

While not always listed in basic glossaries, implied volatility is critical for understanding option pricing. IV represents the market’s expectation of how much the underlying will move over the option’s remaining life. When IV is high (such as before an RBI announcement, budget, or earnings), option premiums are elevated because the market expects larger moves. When IV is low (during calm, range-bound periods), premiums are cheaper. Buying options when IV is unusually high means paying an elevated premium, and if the expected big move doesn’t materialise, the subsequent drop in IV (called “IV crush”) can cause the option to lose value even if the stock moves somewhat in your favour.

When Should You Use a Call and Put Option?

Here’s the simple way to think about it:

Use a Call Option

When you expect the stock price to rise. It allows you to profit from upward movements without buying the stock outright. Calls are most effective when you have a specific bullish view over a defined timeframe. Buying a call without a sense of when the move should happen, and therefore which expiry to choose, often leads to time decay eating into the premium before the anticipated move occurs.

Use a Put Option

When you expect the stock price to fall. It lets you benefit from declines or protect yourself from losses on existing stock holdings. Puts are particularly useful around events that carry downside risk, such as earnings announcements, where you’re uncertain about the outcome but want to protect a position you don’t want to sell.

But options aren’t just for speculation; they’re also a practical hedging tool. For example, if you already hold a stock and are worried about a potential drop, buying a put option acts like insurance for your portfolio. It helps limit your losses while still allowing you to participate in any gains. The cost of the put premium is the “insurance premium” you pay for this protection, and just like insurance, it’s most valuable when purchased before the risk event, not after the decline has already started.

In short, calls are for bullish views, puts are for bearish views, and both can be used strategically to protect or enhance your investment approach.

Common Beginner Mistakes with Options

Buying Deep OTM Options Because They’re “Cheap”

A ₹5 option on Nifty seems affordable, but it requires a very large move in a short time to become profitable. The low absolute cost masks a low probability of success. Over many such trades, the cumulative losses from premiums paid on options that expire worthless can be substantial.

Ignoring Time Decay

Beginners often buy options and then wait passively for the stock to move. Meanwhile, the option loses value every day due to theta decay. If the expected move takes longer than anticipated, the option can lose 30–50% of its value from time decay alone, even if the stock eventually moves in the right direction.

Trading Without Understanding Lot Sizes

On Indian exchanges, options trade in lots (e.g., Nifty lot size is 75 units as of the current contract specifications, though this changes periodically). A premium of ₹100 per unit means the actual cost per lot is ₹7,500. Beginners sometimes enter trades without calculating the total premium at risk in rupee terms, which can lead to position sizes that are larger than intended relative to their trading capital.

Holding Options Through Expiry Week Without a Plan

The final week before expiry, particularly the last two days, sees accelerated time decay and unpredictable price behaviour. Options that are slightly OTM can swing between ₹5 and ₹50 in a matter of hours on expiry day. Having a clear plan for whether to hold, exit, or roll the position before the final week reduces the element of surprise.

Conclusion

Options can seem complicated at first, but once you understand the basics of call and put options, they become practical tools for both trading and risk management.

A call option gives you the right to buy a stock and profits when prices rise, while a put option gives you the right to sell and profits when prices fall. Beyond speculation, options can also act as insurance for your portfolio, helping you hedge against potential losses.

Key concepts like intrinsic value, time value, premium, and time decay (theta) are crucial to understanding how options are priced and how their value changes over time. For beginners, starting with buying ATM or slightly ITM options on highly liquid instruments like Nifty provides the most forgiving learning environment, where the bid-ask spreads are tight and the price behaviour is easier to track against a well-covered underlying index. Knowing these terms and building familiarity through small, well-defined positions helps you make informed decisions and manage risk effectively as you develop your understanding of this versatile instrument.

Frequently Asked Questions (FAQs)

What is the difference between a call and a put option?

A call option gives you the right to buy an asset at a specific price within a set time, useful if you expect prices to rise. A put option gives you the right to sell an asset at a specific price within a set time, useful if you expect prices to fall. Both require paying a premium upfront, and both have a defined expiry date after which they cease to exist. The buyer’s maximum loss in either case is limited to the premium paid.

Can I lose more than the premium?

If you are the buyer of a call or put, your maximum loss is limited to the premium paid for the option. However, if you are selling or writing options, your potential losses can be significantly higher, sometimes even unlimited for naked call sellers if the stock rises sharply. Understanding this distinction between buying and selling risk is essential before placing any option trade. Beginners should generally limit themselves to option buying until they have a thorough understanding of the risk dynamics of selling.

Which is better for beginners, calls or puts?

There is no universally better option; it depends on your market view and risk tolerance. Beginners should first learn the mechanics of both calls and puts, experiment with small positions, and focus on strategies like buying ITM or ATM options to understand profit and loss dynamics before taking bigger risks. Starting with Nifty options rather than stock options provides better liquidity and tighter spreads, which reduces the cost of the learning process. Understanding how time decay affects your position over a few trades is more valuable than trying to optimise strike selection from day one.

Can I sell an option before expiry?

Yes. Most option traders on Indian exchanges close their positions by selling the option in the market before expiry rather than holding to expiration. If the option has gained value since you bought it, you sell it at a higher premium and pocket the difference. If it has lost value, you can sell it to recover whatever premium remains rather than waiting for it to expire worthless. This flexibility to exit at any time during market hours is one of the practical advantages of trading listed options on liquid instruments.

Disclaimer: This content is for educational purposes only and does not constitute financial or investment advice. Investments in securities or other financial instruments are subject to market risk, including partial or total loss of capital. Past performance is not indicative of future results. Always consider your financial situation carefully and consult a licensed financial advisor before making investment or trading decisions.

Table of Content

- Call vs Put Options: Quick Comparison

- What Are Options in the Stock Market?

- Types of Options

- What Is a Call Option?

- What Is a Put Option?

- How to Calculate Call and Put Option Payoffs

- Important Terms Related to Call and Put Options

- When Should You Use a Call and Put Option?

- Common Beginner Mistakes with Options

- Conclusion

- Frequently Asked Questions (FAQs)

Engineered for the obsessed. Built for traders.

Purpose-built terminals.

Zero compromise.

Built for speed.

Plot No 1290, 2nd Floor, 17th Cross, 5th Main, Sector-7, HSR Layout, Bangalore 560102

Follow us on

Mintcap Brokers Private Limited

CIN – U66110KA2023PTC178706 | Registered Address: Plot No 1290, Second Floor, 17th Cross, 5th Main, Sector-7, HSR Layout, Bangalore 560102 | Tel: 080 – 49552310 | Email ID: compliance@capmint.com | SEBI registered Stock Broker: INZ000322732 | NSE Cash/F&O Member ID: 90430 | BSE Cash/F&O Member ID: 6903 | MCX Member ID: 57400 | NCDEX Member ID: 1312 | SEBI registered Depository Participant: IN-DP-806-2025 | CDSL DP ID: 12102300 | NSE Clearing Member code: M70108 | AMFI-Registered Mutual Fund Distributor: ARN-289109 (Valid upto 28-Feb-2027) | Category II Execution Only Platform : E6903

Details of Client Bank Account

Compliance Officer: Ms. Shridevi Vungarala | Email ID: compliance@capmint.com | Tel no. + 91 9035330126 | Grievance Redressal Officer (GRO) – Ms. Shikha Gupta | Email ID: Grievance@capmint.com | Tel no: 9035331595.

Procedure to file a complaint on SEBI SCORES: Register on SCORES portal. Mandatory details for filing complaints on SCORES: Name, PAN, Address, Mobile Number, E-mail ID. Benefits: Effective Communication, Speedy redressal of the grievances. You may refer the website https://scores.sebi.gov.in/ for more information. You may also download the SEBI Scores app to log a complaint Android: https://play.google.com > store > apps > sebiscores iOS: https://apps.apple.com > app > sebiscores

Disclaimer

Investment in the securities market are subject to market risks, read all the related documents carefully before investing. Brokerage will not exceed the SEBI prescribed limit.

Mutual fund investments are subject to market risks, read all scheme related documents carefully before investing. Mutual Funds are not exchange-traded products.

Attention Investor:

- Stock Brokers can accept securities as margin from clients only by way of pledge in the depository system w.e.f. September 1, 2020.

- Update your mobile number & email Id with your stock broker/depository participant and receive OTP directly from depository on your email id and/or mobile number to create pledge.

- Pay 20% as upfront margin of the transaction value to trade in cash market segment.

- Investors may please refer to the Exchange’s Frequently Asked Questions (FAQs) issued vide circular reference NSE/INSP/45191 dated July 31, 2020 and NSE/INSP/45534 dated August 31, 2020 and other guidelines issued from time to time in this regard.

- Check your Securities /MF/ Bonds in the consolidated account statement issued by NSDL/CDSL every month.