Link copied!

Option Writing

Option writing, also known as option selling, is the process of selling a call or put option, where the writer (seller) must fulfil the terms of the contract if the buyer exercises the option.

Key Takeaways

- Option writing involves creating and selling call or put options in exchange for a premium. It’s used to generate regular income but comes with obligations if the buyer exercises the contract.

- Covered writing involves owning the underlying asset (safer), while naked writing doesn’t (riskier). Covered calls and cash-secured puts are popular conservative strategies.

- From earning income in sideways markets to acquiring stocks at a discount, option writing strategies (like covered calls, straddles, and iron condors) can be adapted to various market situations, but require proper risk management.

Understanding Option Writing in Stocks Market

Option writing, also known as selling an option (we will continuously use the term writing instead of selling throughout the article), involves creating and selling an options contract in the market. The writer receives a premium from the buyer in exchange for taking on the obligation to fulfil the contract’s terms if exercised.

There are two main types of options: calls and puts. When writing a call option, the writer must sell the underlying asset if the option is exercised. When writing a put option, the writer must buy the underlying asset if exercised.

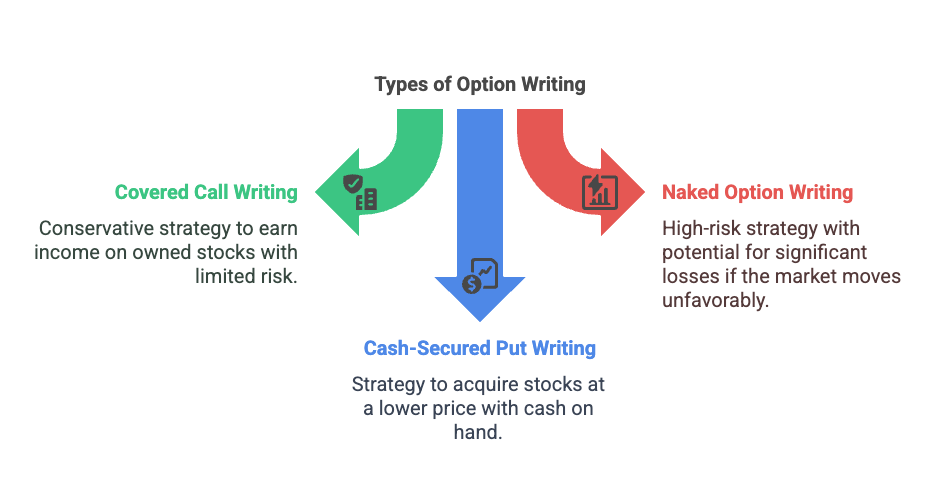

Types of Option Writing

Mainly, there are only two types of option writing, which are called call option writing and put option writing, which can be placed under the naked or uncovered option writing category (which we have covered below). So instead of discussing only these points, which are a bit cliché, we will talk about broader categories such as:

- Covered Call writing

- Naked or Uncovered option writing, and

- Cash-Secured Put Writing

Covered Call Writing

This strategy involves writing call options against a stock you already own. It is a relatively conservative approach and is often used to earn additional income on long-term stock holdings. The risk is limited, as you already own the asset, and the profit comes from the premium received, but you must also note that the upside potential is also limited.

Why? Because when you sell a call option on a stock you own, you’re agreeing to sell your shares at the strike price if the option buyer decides to exercise the option. This caps your maximum selling price, regardless of how high the stock may go.

If this is your first time trying to understand this topic, you must have a lot of questions, but this next simple example may help you with your questions.

Let’s say you own 100 shares of XYZ stock at ₹50. And you are a bit sceptical (since nothing is a guarantee in the stock market) if the stock will move above the ₹50- ₹55 range.

So you write a call (in this case, it would be called a covered call since you already own the stock)

- Strike price: ₹55

- Premium received: ₹2 per share.

Now, there could be two scenarios, the first being that the call option expires above the strike price, let’s say ₹65 and the second scenario being that the call option expires below the strike price, let’s say ₹50.

Scenario 1: The Stock goes to₹65 at expiration

- You must sell your 100 shares at ₹55 (obligation), not ₹65.

- Your total profit will be calculated as follows:

- ₹5 per share on stock ( ₹55 − ₹50) = ₹500

- Plus the ₹200 (₹2*100) premium = ₹700 total

So, instead of making ₹1,500 (15*10), you’re limited to ₹700.

Had the option expired, let’s say at ₹50, you would have received the premium of ₹2 per share, meaning total realised profit of ₹200 and the unrealised capital gain on your stock XYZ of ₹1500.

That’s the opportunity cost of the premium income: if the stock takes off, you don’t get to ride the full rally.

Naked (Uncovered) Option Writing

Unlike in the covered option writing, in this approach, the writer sells options without owning the underlying asset. This can lead to substantial risk because if the market moves unfavourably, the writer may incur significant losses. For instance, writing a naked call exposes the writer to unlimited loss potential if the asset price rises sharply.

Let’s continue our last example and say that the XYZ stock again closed at ₹65, unlike in our last example, where you still got a total payout of ₹700; here, since you don’t own the stock, you will be forced to pay for the stock at ₹55(the strike price you selected)

The Resulting math would look something like:

- You buy 100 shares at ₹65 = –₹6,500

- You sell 100 shares at ₹55 (per the option terms) = +₹5,500

- You received ₹2 per share in premium = +₹200

Which would ultimately leave you with a loss of -₹800 (₹5,500 + ₹200 – ₹6,500).

And in case the option expired below ₹55, you would have only earned ₹200 (the premium amount)

Cash-Secured Put Writing

This involves writing put options while keeping enough cash on hand to purchase the stock if the option is exercised. It is often used by investors looking to acquire a stock at a lower price. The premium received reduces the effective purchase price, making it a prudent strategy in mildly bullish markets.

Let’s continue our example and say that you’re interested in buying XYZ stock if it falls below its CMP of 50, and you’d like to get paid while waiting.

By selling one put option with a strike price of ₹55. For this, you receive a premium of ₹2 per share, or ₹200 in total for the 100-share contract.

Scenario 1: If the stock falls below ₹55, say to ₹50, the put option ends up in the money, and the buyer exercises it. This means you’re obligated to purchase 100 shares of XYZ at ₹55, even though the current market price is only ₹50. While this may seem like a loss, the ₹2 per share premium you received lowers your effective purchase price to ₹53 per share, which is still better than paying ₹55.

Scenario 1: If the stock stays at ₹55 or higher, the put option expires worthless. You keep the full ₹200 premium and walk away without having to buy the stock. In this case, you earned income simply for agreeing to potentially buy the stock, and you can repeat the strategy the following month if you wish.

If you have understood this much, you can easily grasp the strategies based on this Option Writing.

Option Writing Strategies

Let’s break down some smart and practical option writing strategies that real traders use to earn income and manage risk in all kinds of market situations.

Covered Call Strategy

This strategy is best for investors who are moderately bullish on a stock. By holding the stock and selling a call option on it, investors can earn a premium and potentially sell the stock at a profit if the call is exercised. It’s ideal for stable or slightly rising markets.

Protective Put Strategy

Although primarily used by buyers, option writers can benefit by offering protective puts to hedge positions. This strategy involves selling a put while holding the underlying asset or other offsetting positions. It limits downside risk while providing some income from the premium.

Straddle Writing

Straddle writing entails selling both a call and a put option at the same strike price and expiration date. This strategy profits when the underlying asset remains stable, as both options may expire worthless, allowing the writer to keep both premiums. It is best used in low-volatility environments.

Iron Condor Strategy

An iron condor involves selling a call spread and a put spread on the same underlying asset with different strike prices but the same expiration date. This strategy benefits from low volatility, allowing all options to expire worthless, thereby keeping the net premium received.

Benefits of Option Writing

Now, let’s filter out what the benefits of Option Writing are:

- Earn Regular Income: By collecting premiums from selling options, writers can generate a steady stream of income regardless of market direction. This consistent inflow adds predictability to a portfolio, especially in sideways or range-bound markets.

- Buy Stocks at Lower Prices: Writing cash-secured puts can help investors acquire stocks at a discount while earning a premium in the process. It’s a useful approach for long-term investors who prefer to own quality stocks at a lower entry point.

- Adapt to Market Conditions: Option writing strategies can be adjusted based on whether the market is bullish, bearish, or flat, giving traders more flexibility. This allows for creative positioning and better control of risk based on evolving market sentiment.

Risks Involved in Option Writing

While option writing can be rewarding, it’s important to know the risks that could impact your capital and strategy success.

Unlimited Loss Potential:

As already noted in the earlier examples, when writing naked options, especially naked calls, there’s no cap on how much you could lose if the market moves sharply against you.

Market Volatility:

Sudden or unexpected price swings can impact your position significantly, sometimes making it hard to react in time to prevent losses.

Contractual Obligations:

As an option writer, you’re obligated to fulfil the contract if exercised, meaning you may have to buy or sell the asset at a loss if conditions turn unfavourable.

Option Writer vs. Option Buyer

Understanding the roles and responsibilities of option writers versus buyers is essential for grasping how these positions function in a trading scenario. While one takes on an obligation in exchange for income, the other seeks opportunity through rights and limited risk.

|

Feature |

Option Writer |

Option Buyer |

|---|---|---|

|

Role in Contract |

Creates and sells the option to receive a premium from the buyer |

Purchases the option to gain the right to buy or sell the underlying asset |

|

Obligation/Rights |

Legally obligated to fulfil the terms of the contract if exercised |

Holds the right but not the obligation to exercise the contract |

|

Income/Payout |

Earns a fixed premium upfront, regardless of market outcome |

Pays the premium upfront, aiming to profit from favourable price movements |

|

Risk |

Risk can be significant or unlimited, especially with uncovered positions |

Loss is limited to the premium paid for the option |

|

Profit Potential |

Profit is generally capped at the premium received |

Potential for high returns if the asset moves significantly in their favour |

Conclusion

Option writing is a powerful strategy that can enhance income and support diverse market views. However, it demands a deep understanding of the market, risk management, and strategic execution. Traders should evaluate their risk tolerance and market outlook before employing option writing strategies and consider consulting with financial professionals to ensure alignment with investment goals.

Frequently Asked Questions (FAQs)

Is option writing riskier than option buying?

Yes, option writing can be riskier than option buying, especially when done without owning the underlying asset (naked writing). Unlike buyers who risk only the premium paid, writers can face unlimited losses if the market moves sharply against their position.

Can beginners try option writing strategies?

Beginners should start with conservative strategies like covered call writing or cash-secured put writing, where the risks are defined and manageable. It’s important to fully understand how options work before jumping into writing contracts.

Do I need a lot of capital to start writing options?

Option writing, especially cash-secured puts and covered calls, requires a decent capital base. For example, writing one contract typically involves 100 shares, so you need enough funds to either hold the stock or buy it if assigned.

How is profit made through option writing?

Profit comes from the premium received when you sell the option. If the option expires worthless (i.e., the buyer doesn’t exercise it), the writer keeps the full premium as income.

Disclaimer: This content is for educational purposes only and does not constitute financial or investment advice. Investments in securities or other financial instruments are subject to market risk, including partial or total loss of capital. Past performance is not indicative of future results. Always consider your financial situation carefully and consult a licensed financial advisor before making investment or trading decisions.

Engineered for the obsessed. Built for traders.

Purpose-built terminals.

Zero compromise.

Built for speed.

Plot No 1290, 2nd Floor, 17th Cross, 5th Main, Sector-7, HSR Layout, Bangalore 560102

Follow us on

Mintcap Brokers Private Limited

CIN – U66110KA2023PTC178706 | Registered Address: Plot No 1290, Second Floor, 17th Cross, 5th Main, Sector-7, HSR Layout, Bangalore 560102 | Tel: 080 – 49552310 | Email ID: compliance@capmint.com | SEBI registered Stock Broker: INZ000322732 | NSE Cash/F&O Member ID: 90430 | BSE Cash/F&O Member ID: 6903 | MCX Member ID: 57400 | NCDEX Member ID: 1312 | SEBI registered Depository Participant: IN-DP-806-2025 | CDSL DP ID: 12102300 | NSE Clearing Member code: M70108 | AMFI-Registered Mutual Fund Distributor: ARN-289109 (Valid upto 28-Feb-2027) | Category II Execution Only Platform : E6903

Details of Client Bank Account

Compliance Officer: Ms. Shridevi Vungarala | Email ID: compliance@capmint.com | Tel no. + 91 9035330126 | Grievance Redressal Officer (GRO) – Ms. Shikha Gupta | Email ID: Grievance@capmint.com | Tel no: 9035331595.

Procedure to file a complaint on SEBI SCORES: Register on SCORES portal. Mandatory details for filing complaints on SCORES: Name, PAN, Address, Mobile Number, E-mail ID. Benefits: Effective Communication, Speedy redressal of the grievances. You may refer the website https://scores.sebi.gov.in/ for more information. You may also download the SEBI Scores app to log a complaint Android: https://play.google.com > store > apps > sebiscores iOS: https://apps.apple.com > app > sebiscores

Disclaimer

Investment in the securities market are subject to market risks, read all the related documents carefully before investing. Brokerage will not exceed the SEBI prescribed limit.

Mutual fund investments are subject to market risks, read all scheme related documents carefully before investing. Mutual Funds are not exchange-traded products.

Attention Investor:

- Stock Brokers can accept securities as margin from clients only by way of pledge in the depository system w.e.f. September 1, 2020.

- Update your mobile number & email Id with your stock broker/depository participant and receive OTP directly from depository on your email id and/or mobile number to create pledge.

- Pay 20% as upfront margin of the transaction value to trade in cash market segment.

- Investors may please refer to the Exchange’s Frequently Asked Questions (FAQs) issued vide circular reference NSE/INSP/45191 dated July 31, 2020 and NSE/INSP/45534 dated August 31, 2020 and other guidelines issued from time to time in this regard.

- Check your Securities /MF/ Bonds in the consolidated account statement issued by NSDL/CDSL every month.