Table of Content

- Key Takeaways

- What is Gamma In Options Trading?

- How to Calculate Gamma in Options Trading?

- Gamma Values

- Significance Of Gamma In Trading

- Gamma Movement

- 3 ways to manage gamma risk

- Understanding Delta in Gamma Trading

- What Is Gamma Squeeze?

- Limitations of Gamma in Options Trading

- Gamma and Delta-Neutral Strategies

- Impact of Volatility on Gamma

- Conclusion

- Frequently Asked Questions (FAQs)

Link copied!

Gamma in Option Trading

Gamma measures the rate of change of an option’s delta with respect to changes in the underlying asset’s price. Gamma is a second-order derivative in options trading, and it helps traders understand how sensitive delta is to price movements.

Key Takeaways

- Gamma tells us how fast the delta changes when the stock price moves. Delta shows how much an option’s price changes with a ₹1 stock price move, and gamma shows how quickly delta itself changes.

- Gamma is highest when the stock price is near the option’s strike price (ATM) because it is uncertain whether the option will end in profit or not. As the price moves, the delta changes quickly in this zone.

- When gamma is high, delta changes fast, so traders must adjust their positions more often to manage risk. This is called gamma hedging, and it helps avoid sudden losses when stock prices move.

- Sometimes, market makers buy more stock to cover their options, causing the stock price to rise even more. This cycle is called a gamma squeeze and can lead to a sudden price spike.

What is Gamma In Options Trading?

Gamma simply measures how much the delta changes when the underlying moves by a certain number of points. Delta is an order derivative of the underlying, and the rate change of delta is measured by gamma. Then, it is called a second-order derivative with respect to the underlying.

Gamma helps to understand the risk of option contracts in positions because it measures how fast Delta changes as the underlying asset’s price moves. Gamma helps traders understand how sensitive their position is and how precise and frequent their hedging adjustments need to be.

For example, suppose you buy an ATM Nifty Call Option when Nifty is at 22,000.

- Delta is 0.5, meaning if Nifty rises by 1 point, the option gains ₹0.5.

- Gamma is 0.02, meaning for every 1-point move in Nifty, Delta will increase by 0.02.

So, if Nifty moves to 22,001:

- Delta becomes 0.52.

Further moves will impact the option price more because Delta is now bigger.

How to Calculate Gamma in Options Trading?

Gamma measures how much delta changes when the underlying asset price moves by one point. Gamma is calculated by comparing the change in delta with the change in the underlying asset price.

Formula to Calculate the Gamma in Options Trading:

Gamma = Change in Delta / Change in Underlying Asset Price

For example, if delta changes from 0.50 to 0.55 when the stock price rises by ₹5, then:

Gamma = (0.55−0.505) / 5 = 0.01

This means delta changes by 0.01 for every ₹1 movement in the stock price.

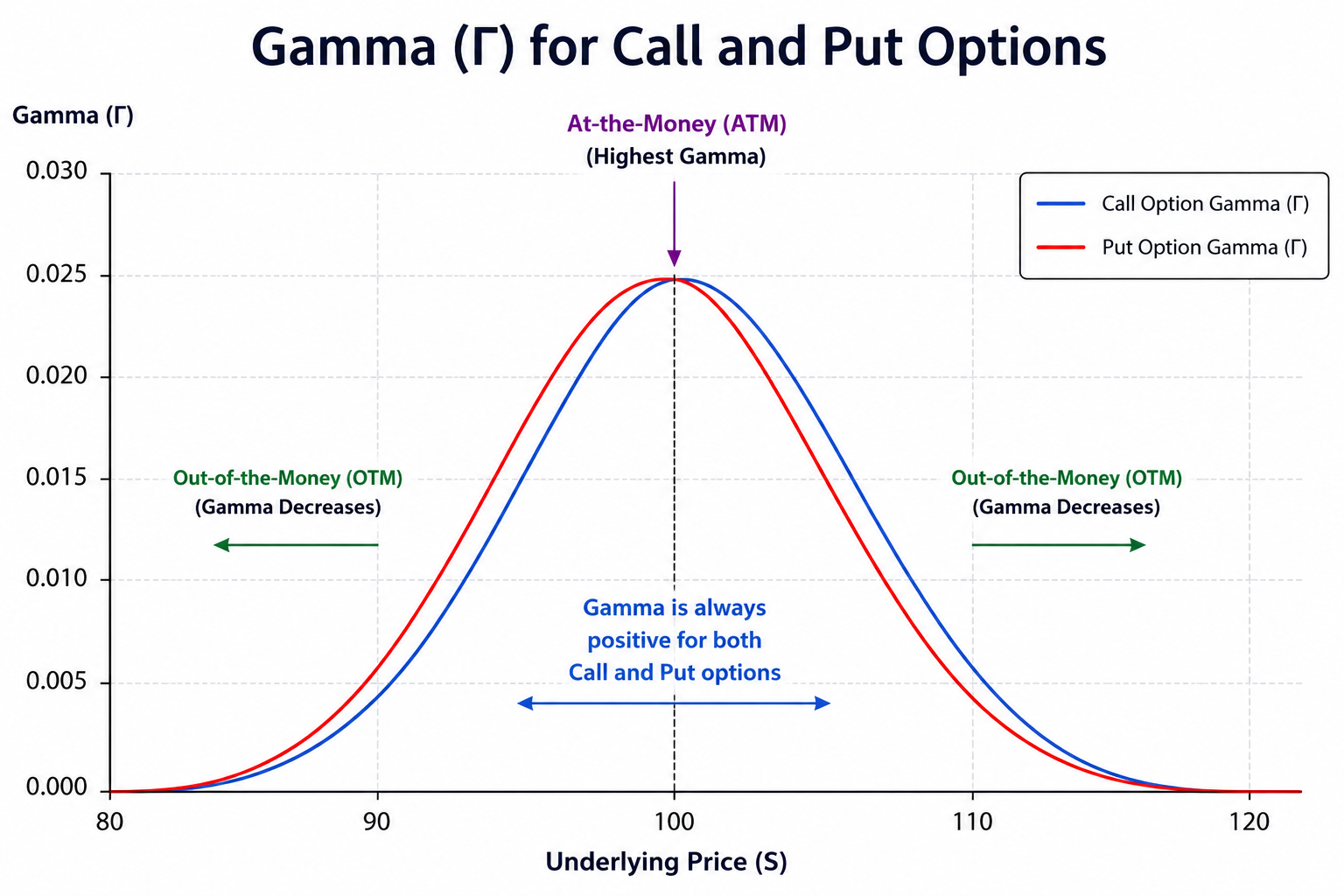

Gamma Values

Just like delta, which ranges from -1 to +1, gamma is always a positive value. This is because gamma shows how much delta will change when the price of the underlying asset moves.

It does not matter whether it is a call option or a put option; gamma behaves the same way for both. It only depends on how close the underlying price is to the strike price. Here’s a graph showing the Gamma values for Call and Put options.

Gamma is higher for at-the-money options because this is the point where it is most uncertain whether the option will end up in profit or not. If the price moves up, the option can quickly become valuable, and if the price moves down, it can become worthless.

Because of this uncertainty, the delta changes quickly when the price is near the strike price. Gamma measures how fast the delta changes, so it is highest at this point of uncertainty.

When an option is deep in the money or deep out of the money, its price is less sensitive to small changes in the price of the underlying asset. This is because delta is already near 1 for deep in-the-money options or near 0 for deep out-of-the-money options.

Significance Of Gamma In Trading

Gamma is also one of the important options for traders, and it also impacts the option prices. Traders often speculate on gamma to adjust their positions accordingly. Here is the explanation of the significance of gamma in trading.

Traders monitor gamma to manage portfolio risk

Gamma tells traders how quickly delta changes when the price of the underlying asset moves.

When gamma is high, delta can change rapidly, which means the position’s risk can increase suddenly. So, traders closely watch gamma to avoid getting caught off guard by sudden price moves.

At the money option contracts near expiry have high gamma because the strike price is very close underlying. Now, your position is much more exposed to Nifty’s price movements. Here, traders adjust their hedges frequently when gamma is high; constant adjustment is called gamma hedging.

Gamma In Trading Strategies

Gamma is important in trading strategies when traders create delta-neutral positions to profit from volatility. Traders use gamma to manage their positions by buying and selling the underlying asset as the price moves. This process is called hedging.

They frequently adjust delta to keep their position neutral. This helps traders benefit from price movements in either direction, whether the price goes up or down, as long as the market is volatile.

Gamma Movement

amma changes depending on the relationship between the stock price, strike price, and time remaining until expiry.

Gamma is usually:

- Highest for At-the-Money (ATM) options

- Lower for deep In-the-Money (ITM) options

- Lower for deep Out-of-the-Money (OTM) options

As expiry approaches, gamma becomes more sensitive, especially for ATM option contracts. Small price movements can rapidly change delta during this period.

3 ways to manage gamma risk

Managing gamma risk is important because rapid changes in delta can significantly affect portfolio exposure.

Maintain Delta-Neutral Positions

Traders often balance positive and negative delta positions to reduce directional exposure and manage gamma risk more effectively.

Adjust Hedging Frequently

When gamma is high, traders may need to adjust their hedges more often because delta changes rapidly with small price movements.

Avoid Excessive Near-Expiry Exposure

ATM options near expiry usually carry very high gamma risk. Many traders reduce exposure near expiration to avoid sudden portfolio fluctuations.

Understanding Delta in Gamma Trading

Delta and gamma are closely connected in options trading. Delta measures how much an option’s price changes when the underlying asset moves, while gamma measures how quickly that delta changes.

When gamma is high, even small movements in the stock or index price can rapidly change delta, making the option position more sensitive to market movements.

What Is Gamma Squeeze?

Many market makers are option sellers, and they don’t want to take on too much risk. So, when they sell call options, they buy the stock to protect themselves from losses if the price goes up.

When a lot of retail traders start buying out-of-the-money (OTM) call options, it creates pressure on market makers. To hedge their risk, market makers start buying the stock. As the stock price starts rising, the value of those options increases, and delta moves up. This forces market makers to buy even more stock to stay protected.

This extra buying pushes the stock price even higher, which again forces more buying from market makers. This cycle can lead to a sharp rise in the stock price. This is called a gamma squeeze because gamma causes delta to change quickly, making market makers buy more and more stock.

Limitations of Gamma in Options Trading

Although gamma is an important Option Greek, it also has certain limitations.

Gamma Changes Continuously

Gamma is not fixed and changes constantly with movements in the underlying asset price, volatility, and time to expiry.

High Gamma Can Increase Trading Costs

Frequent hedge adjustments during high gamma periods may increase brokerage costs and transaction expenses.

Less Useful Without Delta Analysis

Gamma alone cannot fully explain option price behaviour because it only measures the rate of change of delta. Traders usually analyse gamma together with delta and theta.

Rapid Market Movements Increase Risk

Sharp market volatility can cause delta to change aggressively, making gamma-based strategies difficult to manage.

Gamma and Delta-Neutral Strategies

A Delta-neutral strategy is a trading strategy where the overall delta of the portfolio is kept close to zero.

Traders use gamma to manage these positions because delta changes continuously as the underlying asset price moves. When gamma is high, traders may need to rebalance their positions more frequently to maintain delta neutrality and control risk exposure.

Impact of Volatility on Gamma

Volatility significantly affects gamma behaviour in options trading.

During periods of high volatility, option premiums and delta values can change rapidly, increasing the impact of gamma on option positions. Traders closely monitor volatility because sudden market movements can lead to sharp changes in portfolio risk.

Conclusion

Gamma is a crucial option Greek that measures the rate of change in delta concerning the underlying asset’s price movements. It is a second-order derivative that helps traders understand how sensitive their option’s delta is as the market fluctuates. Gamma is highest for at-the-money (ATM) options and increases as expiration nears, indicating rapid changes in delta with small price movements. This makes gamma essential for traders managing delta-neutral strategies and hedging risks effectively. When gamma is high, especially near expiry, traders must frequently adjust their positions to avoid sudden exposure to price swings.

Gamma also plays a pivotal role in market events like a gamma squeeze, where rising option demand forces market makers to buy more stock, driving prices higher. Understanding gamma helps traders navigate volatility, optimise their hedging strategies, and minimise portfolio risk. Monitoring gamma allows for better decision-making in options trading, ensuring both profitability and protection against unpredictable market shifts.

Frequently Asked Questions (FAQs)

What is Gamma in Options Greek?

Gamma measures how quickly delta changes when the price of the underlying asset moves. It helps traders understand how sensitive their option position is to market price changes.

How to calculate gamma in call options?

Gamma in call options is calculated by dividing the change in delta by the change in the underlying asset price.

If delta changes from 0.40 to 0.50 after a ₹10 rise in the stock price, the gamma will be:

Gamma = 0.50−0.40/10 = 0.01

Can we use Gamma to Predict Price Movement in Options Trading?

Gamma itself does not predict market direction, but it helps traders understand how rapidly delta and option sensitivity may change with price movement.

High gamma generally indicates that option prices may react sharply to even small changes in the underlying asset price.

What is the difference between gamma and Delta in finance?

Gamma shows how much delta will change if the stock price moves by ₹1. Delta measures the option’s price sensitivity, while gamma measures how fast delta changes.

What is the gamma strategy?

A gamma strategy is when traders adjust their position frequently to manage delta risk and profit from market volatility. This is called gamma scalping, where traders buy low and sell high as prices move, trying to stay delta-neutral and benefit from price swings.

Disclaimer: This content is for educational purposes only and does not constitute financial or investment advice. Investments in securities or other financial instruments are subject to market risk, including partial or total loss of capital. Past performance is not indicative of future results. Always consider your financial situation carefully and consult a licensed financial advisor before making investment or trading decisions.

Table of Content

- Key Takeaways

- What is Gamma In Options Trading?

- How to Calculate Gamma in Options Trading?

- Gamma Values

- Significance Of Gamma In Trading

- Gamma Movement

- 3 ways to manage gamma risk

- Understanding Delta in Gamma Trading

- What Is Gamma Squeeze?

- Limitations of Gamma in Options Trading

- Gamma and Delta-Neutral Strategies

- Impact of Volatility on Gamma

- Conclusion

- Frequently Asked Questions (FAQs)

Engineered for the obsessed. Built for traders.

Purpose-built terminals.

Zero compromise.

Built for speed.

Plot No 1290, 2nd Floor, 17th Cross, 5th Main, Sector-7, HSR Layout, Bangalore 560102

Follow us on

Mintcap Brokers Private Limited

CIN – U66110KA2023PTC178706 | Registered Address: Plot No 1290, Second Floor, 17th Cross, 5th Main, Sector-7, HSR Layout, Bangalore 560102 | Tel: 080 – 49552310 | Email ID: compliance@capmint.com | SEBI registered Stock Broker: INZ000322732 | NSE Cash/F&O Member ID: 90430 | BSE Cash/F&O Member ID: 6903 | MCX Member ID: 57400 | NCDEX Member ID: 1312 | SEBI registered Depository Participant: IN-DP-806-2025 | CDSL DP ID: 12102300 | NSE Clearing Member code: M70108 | AMFI-Registered Mutual Fund Distributor: ARN-289109 (Valid upto 28-Feb-2027) | Category II Execution Only Platform : E6903

Details of Client Bank Account

Compliance Officer: Ms. Shridevi Vungarala | Email ID: compliance@capmint.com | Tel no. + 91 9035330126 | Grievance Redressal Officer (GRO) – Ms. Shikha Gupta | Email ID: Grievance@capmint.com | Tel no: 9035331595.

Procedure to file a complaint on SEBI SCORES: Register on SCORES portal. Mandatory details for filing complaints on SCORES: Name, PAN, Address, Mobile Number, E-mail ID. Benefits: Effective Communication, Speedy redressal of the grievances. You may refer the website https://scores.sebi.gov.in/ for more information. You may also download the SEBI Scores app to log a complaint Android: https://play.google.com > store > apps > sebiscores iOS: https://apps.apple.com > app > sebiscores

Disclaimer

Investment in the securities market are subject to market risks, read all the related documents carefully before investing. Brokerage will not exceed the SEBI prescribed limit.

Mutual fund investments are subject to market risks, read all scheme related documents carefully before investing. Mutual Funds are not exchange-traded products.

Attention Investor:

- Stock Brokers can accept securities as margin from clients only by way of pledge in the depository system w.e.f. September 1, 2020.

- Update your mobile number & email Id with your stock broker/depository participant and receive OTP directly from depository on your email id and/or mobile number to create pledge.

- Pay 20% as upfront margin of the transaction value to trade in cash market segment.

- Investors may please refer to the Exchange’s Frequently Asked Questions (FAQs) issued vide circular reference NSE/INSP/45191 dated July 31, 2020 and NSE/INSP/45534 dated August 31, 2020 and other guidelines issued from time to time in this regard.

- Check your Securities /MF/ Bonds in the consolidated account statement issued by NSDL/CDSL every month.