Table of Content

- Key Takeaways

- What is the Strike Price in Options?

- The Relationship Between Strike Price and the Underlying Security

- Moneyness: The Three Types of Strike Prices

- Strike Price and Option Delta

- How to Choose the Strike Price for Options

- Putting It Together: Strike Selection by Strategy

- Conclusion

- Frequently Asked Questions (FAQs)

Link copied!

Strike Price in Options

The strike price is the fixed price at which you can buy or sell the underlying asset if you choose to exercise the option.

Key Takeaways

- Strike price is the fixed price at which an option can be exercised to buy or sell the underlying asset.

- In regular options trading, the strike price and exercise price are typically the same and used interchangeably.

- In some cases, like employee stock options, the strike price is pre-decided, while the exercise price may refer to the actual execution price.

- “Strike off price” is not a standard term in options trading and is often a misused or informal phrase.

What is the Strike Price in Options?

The strike price in options is a key element in every options contract. It refers to the pre-decided price at which the option holder has the right to buy (in the case of a call option) or sell (in the case of a put option) the underlying asset. This price remains fixed throughout the life of the option and does not change regardless of how the market moves. It acts as the reference point for determining whether the option is profitable or not at any given time.

The relationship between the strike price and the current market price determines the intrinsic value of the option. If the market moves in a favourable direction relative to the strike price, the option gains value; if not, it may expire worthless. Understanding the strike price is essential for analysing risk, potential reward, and choosing the right strategy in options trading.

On Indian exchanges, Nifty options are available at strike intervals of 50 points (e.g., 22,000, 22,050, 22,100), while Bank Nifty options have 100-point intervals. Stock options have varying intervals depending on the stock’s price level. This granularity gives traders a wide range of strike prices to choose from, but it also means that selecting the right one requires a clear framework rather than picking randomly from a long list.

The Relationship Between Strike Price and the Underlying Security

The strike price and the market price of the underlying security are in constant dialogue; they define whether an option holds value and how traders position themselves. This relationship determines whether an option is “in the money,” “at the money,” or “out of the money.” If the market price moves favourably beyond the strike, the option starts gaining real, usable value. If not, it remains speculative or loses its edge. This isn’t just theory; it affects how options are priced, how much premium they carry, and whether they’re worth exercising at all.

But beyond value, this relationship influences strategy and timing. When traders expect the underlying asset to move sharply, they choose strike prices that reflect both risk tolerance and potential payoff. A strike price far from the current market level might offer bigger returns, but only if the market moves fast and far enough. The further the strike is from the current price, the cheaper the option but the lower the probability of it finishing in the money. This trade-off between cost and probability is at the heart of every strike price decision.

A useful way to think about it: the premium you pay for an option is essentially the market’s estimate of the probability that the option will have value at expiry, multiplied by the expected value if it does. A ₹5 out-of-the-money option isn’t cheap because the market is ignoring it; it’s cheap because the market assigns a low probability to the underlying reaching that strike before expiry.

Moneyness: The Three Types of Strike Prices

In options trading, moneyness describes the relationship between the strike price and the current market price of the underlying asset. There are three types: In-the-Money (ITM), At-the-Money (ATM), and Out-of-the-Money (OTM).

For call options, a strike price lower than the market price is ITM, equal to the market price is ATM, and higher than the market price is OTM. For put options, it’s the opposite: a strike price higher than the market price is ITM, equal is ATM, and lower is OTM. Moneyness helps traders understand whether an option has intrinsic value and how likely it is to be profitable.

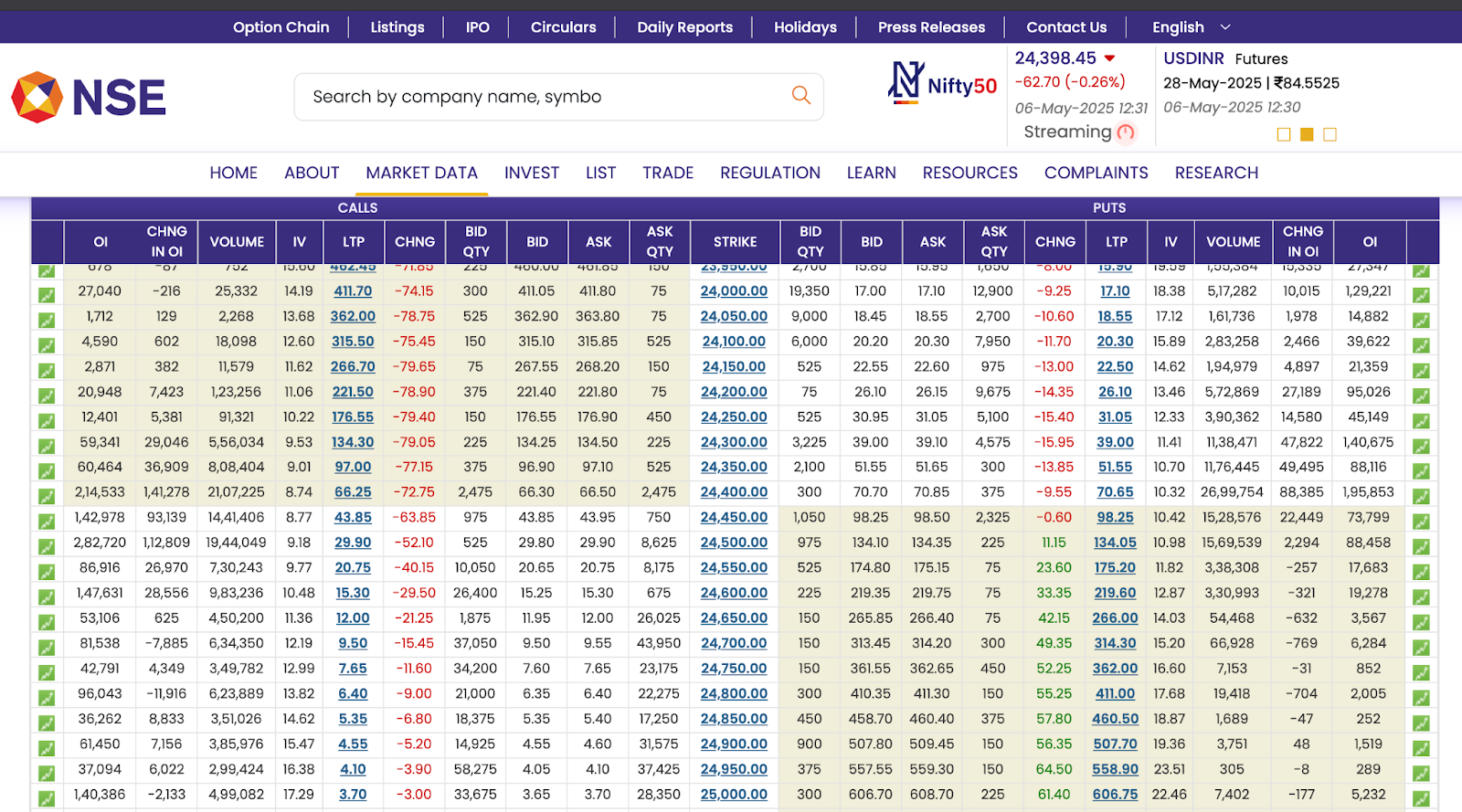

Example from the Nifty Option Chain

Assuming Nifty is trading around 24,400.

Call Options:

- Strikes like 24,300, 24,250, 24,100 are In-the-Money (ITM) — they let you buy below the market price.

- 24,400 strike is At-the-Money (ATM) — it’s closest to the current market price.

- Strikes like 24,450, 24,500, 24,600 are Out-of-the-Money (OTM) — they let you buy at a higher price than the market.

Put Options:

- Strikes like 24,500, 24,450 are In-the-Money (ITM), 24,400 is At-the-Money (ATM), and 24,300, 24,250, 24,100 are Out-of-the-Money (OTM).

Looking at the option chain, you’ll notice that ITM options carry higher premiums because they already have intrinsic value built in. OTM options are cheaper because their entire value is time value and volatility premium, with no intrinsic value. This is immediately visible when you scan any Nifty option chain: the 24,100 call (deep ITM when Nifty is at 24,400) might be priced at ₹320–350, while the 24,600 call (OTM) might be just ₹40–60. The price difference reflects the probability and intrinsic value embedded in each strike.

Strike Price and Option Delta

Delta tells us how much an option’s price will move when the underlying asset moves by ₹1. It also gives a rough idea of the chance that the option will expire in the money. This value is directly influenced by the strike price; the closer the strike is to the current market price, the higher the delta for calls (or the more negative for puts). Here’s how delta typically changes with different strike positions:

| Strike Price Position | Delta (Call Option) | Delta (Put Option) | Meaning |

|---|---|---|---|

| Deep In-the-Money (ITM) | 0.8 to 1.0 | −0.8 to −1.0 | Very high chance of expiring ITM; behaves almost like the underlying asset. |

| At-the-Money (ATM) | Around 0.5 | Around −0.5 | 50-50 chance of finishing ITM; most sensitive to price changes. |

| Out-of-the-Money (OTM) | 0.1 to 0.3 | −0.1 to −0.3 | Low chance of expiring ITM; cheaper but needs a big move to become profitable. |

| Deep Out-of-the-Money (far OTM) | Near 0.0 | Near 0.0 | Very unlikely to finish ITM; priced mostly on time and volatility. |

Delta is one of the most practical Greeks for strike selection. If you buy a call option with a delta of 0.3, you’re essentially saying you believe there’s roughly a 30% chance (as implied by current market pricing) that the option will finish in the money, and you’re comfortable with that probability in exchange for the lower premium. An ATM option with 0.5 delta costs more but gives you a coin-flip probability of profitability.

Delta also changes as the market moves, a concept known as gamma. An OTM option with a delta of 0.15 today might have a delta of 0.45 tomorrow if the underlying moves sharply toward the strike. This acceleration is what produces the large percentage gains that attract speculative option buyers. Conversely, if the market moves away from the strike, delta shrinks further, and the option loses value faster as it becomes increasingly unlikely to finish in the money.

How to Choose the Strike Price for Options

Choosing the right strike price is one of the most important decisions in options trading. It directly affects your cost, risk, probability of profit, and potential return. Here is a practical five-step framework:

Step 1: Define Your Market Outlook

Determine whether you expect the underlying asset to move up, down, or remain sideways. Your directional view is the starting point for every strike price decision. A strongly bullish view calls for a different strike selection than a mildly bullish one. If you expect Nifty to rise 300 points in the next week, you might look at strikes 100–200 points above the current level. If you expect a modest 50–100 point rise, an ATM or slightly OTM strike is more appropriate.

Step 2: Identify Your Role – Buyer or Seller

Clarify whether you plan to buy or sell options, as this fundamentally changes how you approach strike selection.

Option buyers benefit from larger moves and typically choose ATM or slightly OTM strikes for the best balance of cost and probability. Option sellers benefit from time decay and typically sell OTM strikes where they collect premium and profit if the underlying stays away from the strike. For sellers, the further OTM the strike, the lower the premium collected but the higher the probability that the option expires worthless in their favour.

Step 3: Assess Your Risk-Reward Preference

Decide how much risk you are willing to take for potential return. This is where your trading personality matters.

Conservative traders tend to choose ITM or ATM strikes. These cost more but have higher deltas and greater probability of finishing profitable. Aggressive traders may prefer OTM strikes for their lower cost and higher percentage return potential, accepting that many of these trades will result in a total loss of premium. A practical approach is to calculate the breakeven point for each strike you’re considering. If the breakeven requires a move that seems unrealistic given the stock’s typical range, the strike is probably too far out of the money for a reasonable trade.

Step 4: Evaluate Time to Expiry and Volatility

Check how many days are left until expiry and assess current volatility conditions.

With more time to expiry, OTM strikes become more viable because there are more trading sessions for the underlying to move. With weekly options expiring in 2–3 days, OTM strikes face severe time decay and need an immediate, sharp move to be profitable. Volatility also matters: in high-volatility environments, premiums across all strikes are elevated, which means even OTM options are relatively expensive. In low-volatility periods, premiums are cheaper, making it a better time to buy options but also meaning the expected move is smaller.

As a rough guideline for Nifty weekly options: with 4–5 days to expiry, strikes within 200–300 points of the current level are typically the most actively traded and offer a reasonable balance of cost and probability. With only 1–2 days remaining, ATM and the first one or two OTM strikes concentrate most of the meaningful trading activity.

Step 5: Check Liquidity and Volume at Your Chosen Strike

Before finalising, verify that the strike you’ve selected has adequate trading volume and tight bid-ask spreads.

On Nifty and Bank Nifty, ATM and the nearby two to three strikes on either side are typically very liquid, with bid-ask spreads of ₹0.50–2. Further OTM or deep ITM strikes can have wider spreads, sometimes ₹5–10, which directly eats into profitability. On stock options, liquidity drops off more sharply as you move away from ATM. A stock option with a bid of ₹12 and an ask of ₹18 means you’re losing roughly 25% of the midpoint value just to enter the trade. Always check the bid-ask spread before placing an order, particularly on stock options and far OTM strikes.

Putting It Together: Strike Selection by Strategy

| Strategy | Typical Strike Choice | Rationale |

|---|---|---|

| Long Call (Bullish) | ATM or 1–2 strikes OTM | Balance of cost and probability; reasonable breakeven |

| Long Put (Bearish) | ATM or 1–2 strikes OTM | Same logic as long call, applied to downside view |

| Protective Put (Hedging) | 5–7% OTM | Lower cost; absorbs minor declines, protects against larger drops |

| Covered Call (Income) | 3–5% OTM | Allows some upside; premium provides income if stock stays below strike |

| Bull Call Spread | Buy ATM, Sell 2–3 strikes OTM | Reduces net cost; caps profit at the sold strike |

| Straddle (Volatility) | ATM for both call and put | Maximum sensitivity to movement in either direction |

Conclusion

Selecting the right strike price in options trading is a strategic decision that depends on your market view, risk appetite, and whether you’re buying or selling options. The strike price directly impacts the option’s delta, moneyness, and overall profitability. A clear understanding of how it interacts with the underlying asset’s price helps you gauge the potential payoff and risk.

Whether you choose ITM, ATM, or OTM, the strike should align with your trading goals and market expectations. The most common mistake among retail options traders on Indian exchanges is defaulting to the cheapest available strike because the premium is low, without considering that the probability of that strike becoming profitable is equally low. A ₹5 option that has a 5% chance of paying off is not inherently better than a ₹100 option with a 55% chance, even though the absolute cost is much lower.

Always consider time to expiry, volatility, and liquidity before finalising your strike, as these factors significantly influence your success in options trading. The five-step framework outlined above provides a structured way to approach this decision consistently, rather than making ad-hoc choices trade by trade.

Frequently Asked Questions (FAQs)

What is the meaning of strike price in trading?

The strike price is the fixed price at which the buyer of an option can buy (in a call option) or sell (in a put option) the underlying asset. It’s the agreed-upon price mentioned in the options contract, and it helps determine whether an option is profitable (in-the-money) or not. The strike price remains constant for the life of the contract; it is the market price that moves around it.

How is the strike price calculated?

The strike price isn’t calculated by traders; it’s predefined by the exchange at fixed intervals. For Nifty, strikes are set at every 50-point interval; for Bank Nifty, at every 100-point interval. Traders choose from these available strikes based on their strategy, selecting ATM, ITM, or OTM strikes depending on their market view, risk tolerance, and expected price movement.

How to determine the strike price for options?

Determine the strike price by first defining your market outlook and then matching it to your risk-reward preference. Choose ATM for balanced trades with moderate cost and reasonable probability, ITM for higher probability but greater upfront cost, or OTM for lower cost and higher potential percentage returns at the expense of lower probability. Factor in time to expiry, current volatility levels, and the liquidity at your chosen strike before finalising. The breakeven point, calculated as strike price plus premium for calls or strike price minus premium for puts, should represent a realistic target given the underlying’s typical movement range.

What is the difference between the strike price and the exercise price?

In most cases, strike price and exercise price mean the same thing — the price at which the underlying asset can be bought or sold as per the option contract. However, in some contexts, especially in employee stock options (ESOPs), the strike price refers to the pre-set price when the options are granted, while the exercise price may refer to the price at which the employee actually exercises the options, which could differ if the scheme includes adjustments for corporate actions. For regular stock and index options trading on Indian exchanges, both terms are used interchangeably and refer to the same price.

What is the strike-off price?

The term “strike off price” is not used in standard options trading terminology. It’s often confused with strike price. If you came across this term, it might be a typographical error, or used informally in another context like auctions or product clearance sales. It has no recognised meaning in the context of financial derivatives or options contracts.

Disclaimer: This content is for educational purposes only and does not constitute financial or investment advice. Investments in securities or other financial instruments are subject to market risk, including partial or total loss of capital. Past performance is not indicative of future results. Always consider your financial situation carefully and consult a licensed financial advisor before making investment or trading decisions.

Table of Content

- Key Takeaways

- What is the Strike Price in Options?

- The Relationship Between Strike Price and the Underlying Security

- Moneyness: The Three Types of Strike Prices

- Strike Price and Option Delta

- How to Choose the Strike Price for Options

- Putting It Together: Strike Selection by Strategy

- Conclusion

- Frequently Asked Questions (FAQs)

Engineered for the obsessed. Built for traders.

Purpose-built terminals.

Zero compromise.

Built for speed.

Plot No 1290, 2nd Floor, 17th Cross, 5th Main, Sector-7, HSR Layout, Bangalore 560102

Follow us on

Mintcap Brokers Private Limited

CIN – U66110KA2023PTC178706 | Registered Address: Plot No 1290, Second Floor, 17th Cross, 5th Main, Sector-7, HSR Layout, Bangalore 560102 | Tel: 080 – 49552310 | Email ID: compliance@capmint.com | SEBI registered Stock Broker: INZ000322732 | NSE Cash/F&O Member ID: 90430 | BSE Cash/F&O Member ID: 6903 | MCX Member ID: 57400 | NCDEX Member ID: 1312 | SEBI registered Depository Participant: IN-DP-806-2025 | CDSL DP ID: 12102300 | NSE Clearing Member code: M70108 | AMFI-Registered Mutual Fund Distributor: ARN-289109 (Valid upto 28-Feb-2027) | Category II Execution Only Platform : E6903

Details of Client Bank Account

Compliance Officer: Ms. Shridevi Vungarala | Email ID: compliance@capmint.com | Tel no. + 91 9035330126 | Grievance Redressal Officer (GRO) – Ms. Shikha Gupta | Email ID: Grievance@capmint.com | Tel no: 9035331595.

Procedure to file a complaint on SEBI SCORES: Register on SCORES portal. Mandatory details for filing complaints on SCORES: Name, PAN, Address, Mobile Number, E-mail ID. Benefits: Effective Communication, Speedy redressal of the grievances. You may refer the website https://scores.sebi.gov.in/ for more information. You may also download the SEBI Scores app to log a complaint Android: https://play.google.com > store > apps > sebiscores iOS: https://apps.apple.com > app > sebiscores

Disclaimer

Investment in the securities market are subject to market risks, read all the related documents carefully before investing. Brokerage will not exceed the SEBI prescribed limit.

Mutual fund investments are subject to market risks, read all scheme related documents carefully before investing. Mutual Funds are not exchange-traded products.

Attention Investor:

- Stock Brokers can accept securities as margin from clients only by way of pledge in the depository system w.e.f. September 1, 2020.

- Update your mobile number & email Id with your stock broker/depository participant and receive OTP directly from depository on your email id and/or mobile number to create pledge.

- Pay 20% as upfront margin of the transaction value to trade in cash market segment.

- Investors may please refer to the Exchange’s Frequently Asked Questions (FAQs) issued vide circular reference NSE/INSP/45191 dated July 31, 2020 and NSE/INSP/45534 dated August 31, 2020 and other guidelines issued from time to time in this regard.

- Check your Securities /MF/ Bonds in the consolidated account statement issued by NSDL/CDSL every month.