Table of Content

Link copied!

Law of Diminishing Marginal Returns

The Law of Diminishing Marginal Returns states that as you continue to add units of a variable input (like labour) to fixed inputs (like land or machinery), the additional output (or marginal return) produced from each unit of the variable input will eventually decrease.

Key Takeaways

- The law of diminishing marginal returns explains that adding more of a variable input to fixed resources eventually leads to reduced efficiency and smaller output gains.

- It helps businesses identify the optimal level of input use, avoid overproduction, and manage costs effectively.

- The concept is essential in short-run production analysis and plays a key role in shaping decisions on resource allocation, labour planning, and investment in technology.

Define Law of Diminishing Marginal Returns

The Law of Diminishing Marginal Returns is an important concept in production economics. It states that when you keep adding more of a variable input, such as labour, to fixed inputs like land, machines, or tools, the extra output produced by each new unit of input will eventually begin to decline. In the beginning, adding more workers may increase total production significantly because they can specialise and work efficiently. However, after a certain point, there are too many workers and not enough machines or space, causing overcrowding and inefficiency.

As a result, the benefit of adding each extra worker becomes smaller, even though total output may still increase. Eventually, if too many workers are added, total output might even decline. This law helps businesses understand how to balance their resources for maximum productivity. It shows that more is not always better and that efficiency requires the right mix of inputs.

Importance in Economic Theory and the Production Function

The Law of Diminishing Marginal Returns plays a vital role in economic theory, particularly in understanding how businesses make production decisions. It highlights the point at which adding more of a variable input, such as labour, yields progressively smaller increases in output, guiding firms toward the most efficient use of their resources.

This concept is essential in shaping production functions, optimising input combinations, and determining cost structures. It influences a wide range of business strategies, including workforce planning, investment in machinery, and pricing decisions. By recognising the limits of productivity, firms can avoid inefficiencies, reduce waste, and improve overall profitability.

Why Diminishing Returns Happen?

The Law of Diminishing Marginal Returns occurs because some resources remain fixed in the short run. While businesses can easily increase variable inputs like labour or raw materials, they cannot immediately expand fixed resources such as factory space, machinery, or land. As more variable inputs are added to the same fixed resources, those resources become overcrowded and less efficient.

Initially, additional workers improve productivity by sharing tasks and specialising in different activities. However, once the available machinery or workspace reaches its capacity, each additional worker has fewer resources to work with. This reduces the extra output generated by every new unit of input.

In simple terms, diminishing returns happen because increasing one factor of production while keeping others constant eventually creates inefficiencies. Businesses can delay this stage through better technology, improved processes, or expanding their fixed resources, but they cannot eliminate the principle in the short run.

The Mechanism Behind Diminishing Returns

Understanding how diminishing marginal returns work is crucial to managing inputs effectively in any production process. When a firm increases one input (like labour) while keeping other inputs (like machinery or space) constant, total output initially rises. In the early stages, additional input can lead to more efficient production as tasks are shared and workers collaborate. However, after a certain point, adding more input leads to overcrowding or inefficiencies, causing the rate of output growth to slow down. This is when diminishing marginal returns set in.

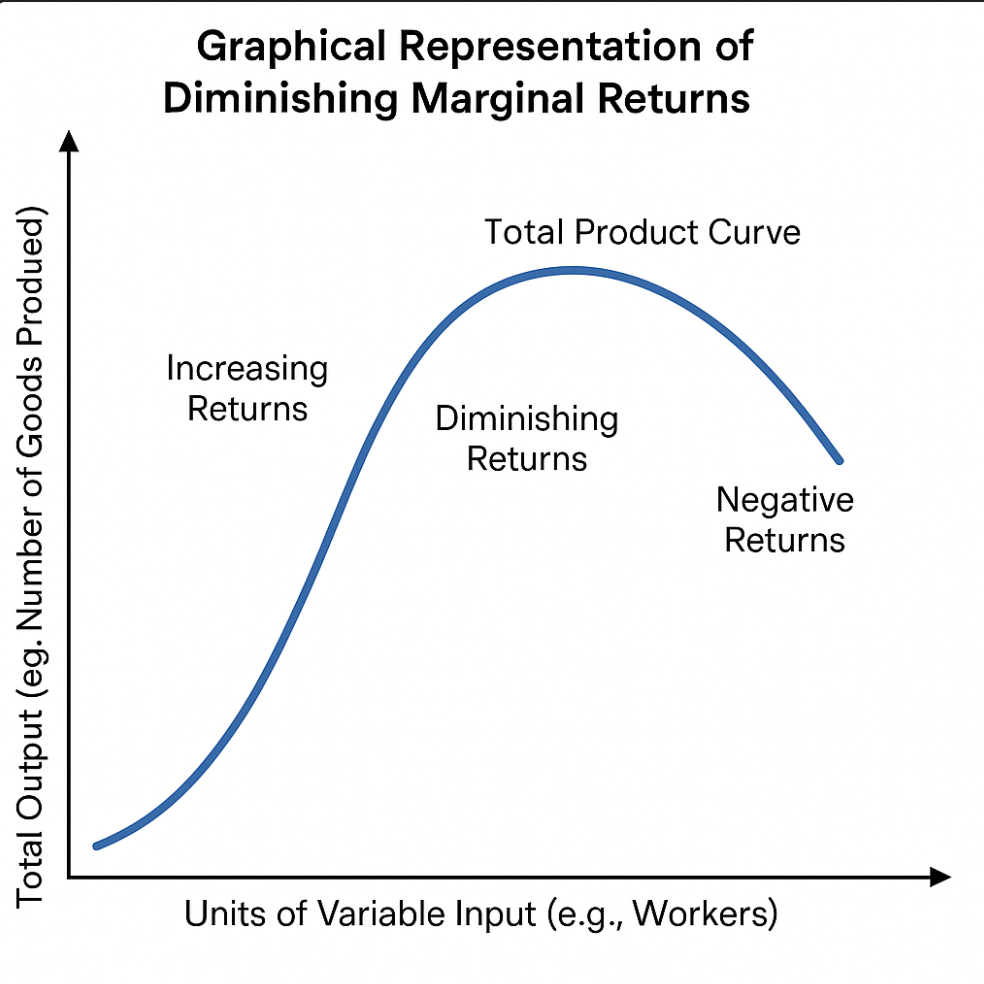

Graphical Representation of Diminishing Marginal Returns

This concept is best understood through a graph where the x-axis represents the units of a variable input (e.g., labour), and the y-axis represents total output. The total product curve rises steeply at first, then starts to slope upward more slowly, eventually flattening or even declining. This shape clearly shows how each added input contributes less to the total output after a certain point.

Examples

- Agriculture: A farmer applying fertiliser to a fixed area of land will see yield increases initially. However, too much fertiliser can damage the soil or the crops themselves, leading to reduced output despite higher input.

- Manufacturing: In a production facility with one machine, adding more workers can boost output at first. But once the optimal number is exceeded, workers may crowd each other, reduce efficiency, or even slow down the process, leading to diminishing returns.

How does the law of Diminishing Marginal Returns work?

The law works in three distinct stages as a business increases the amount of a variable input while keeping fixed inputs constant.

Stage 1: Increasing Returns

In the initial stage, adding more workers or other variable inputs increases productivity rapidly. Employees can divide tasks more efficiently, utilise machinery better, and improve coordination. As a result, both total output and marginal output increase.

Stage 2: Diminishing Returns

After reaching an optimal level of production, each additional worker contributes less to total output than the previous one. Although production continues to increase, the rate of growth slows because fixed resources like machines or factory space become limited. This is the stage where the Law of Diminishing Marginal Returns begins to operate.

Stage 3: Negative Returns

If the business continues adding more inputs beyond the optimal point, overcrowding and inefficiencies become severe. Workers compete for the same equipment or workspace, causing productivity to decline. Eventually, total output may even decrease despite employing more resources.

For example, imagine a bakery with four ovens. Hiring more bakers initially increases production because all ovens are used efficiently. However, hiring too many bakers means several workers must wait to use the same ovens, reducing productivity. Eventually, overcrowding slows the entire production process.

History of Diminishing Returns

The concept of diminishing returns has been part of economic theory for more than two centuries. It was first developed by classical economists while studying agricultural production, where land was considered a fixed resource.

One of the earliest economists to explain this principle was Anne Robert Jacques Turgot in the 18th century. Later, economists such as David Ricardo, Thomas Robert Malthus, and John Stuart Mill expanded the concept to explain how increasing labour on a fixed piece of land eventually produces smaller increases in agricultural output.

During the Industrial Revolution, the law was extended beyond agriculture to manufacturing and other industries. Economists realised that the same principle applied whenever one production factor remained fixed while another kept increasing.

Today, the Law of Diminishing Marginal Returns is a fundamental concept in microeconomics, production theory, business management, and operations planning. Companies use it to determine the optimal combination of labour, capital, and technology to maximise productivity while minimising costs.

Key Factors Influencing Diminishing Returns

While the Law of Diminishing Marginal Returns is a general principle, its onset and impact can vary based on several factors. Understanding these variables helps businesses better manage inputs, reduce inefficiencies, and sustain productivity for longer periods. Below are some of the key factors that influence how and when diminishing returns set in:

Role of Resource Allocation in Production Efficiency

Efficient input management is essential for maximising output. A well-balanced combination of labour, machinery, and materials can help delay diminishing returns and ensure smoother, more productive operations.

Impact of Technology on Diminishing Returns

Technological improvements can extend the productive capacity of fixed inputs. Advanced machinery, automation, and smarter processes allow businesses to utilise variable inputs more effectively, pushing the point of diminishing returns further out.

Differences in Short-term vs Long-term Perspectives

In the short run, businesses operate with some fixed inputs, making them more susceptible to diminishing returns. In the long run, however, investments in training, infrastructure, and technology can reduce or even overcome these limitations, leading to more sustainable growth.

Conclusion

The Law of Diminishing Marginal Returns is a practical tool for identifying the limits of productive efficiency. It helps businesses recognise when increasing input no longer leads to proportional output gains. This insight is vital for optimising resource allocation, setting realistic production goals, and avoiding unnecessary costs due to overcrowding or underutilization of fixed assets. By monitoring when returns begin to diminish, firms can adjust input levels, invest strategically in technology, and maintain operational balance, ensuring that growth efforts are both cost-effective and sustainably aligned with long-term productivity goals.

Frequently Asked Questions (FAQs)

What is the law of diminishing marginal returns in detail?

The law of diminishing marginal returns states that if additional units of a variable input (such as labour) are added to fixed inputs (like land or machinery), the marginal output from each new unit of the variable input will eventually decrease. Initially, output may rise at an increasing rate, but after a certain point, each added input contributes less and less to overall production. This decline occurs due to limitations in fixed resources, which leads to overcrowding or inefficiencies in the production process.

What does the law of diminishing marginal returns refer to?

It refers to the point in production where adding more of a variable input leads to smaller increases in output. While total output may still rise, the rate of increase slows down. This concept highlights the importance of balanced resource use and helps businesses identify the most productive input combinations.

What is an example of the law of diminishing returns?

In a factory with one machine, hiring more workers initially boosts production because tasks can be divided. However, after reaching an optimal number, each additional worker has less space and access to the machine, causing productivity per worker to decline. Eventually, adding more workers may even lower total output due to overcrowding.

What is the law of diminishing marginal returns in IB Economics?

In IB Economics, this law is introduced as part of the theory of production in microeconomics. It explains how, in the short run, the productivity of a variable input declines as more is used with fixed resources. The concept is critical in analysing cost behaviour, production efficiency, and the structure of the short-run production function.

Disclaimer: This content is for educational purposes only and does not constitute financial or investment advice. Investments in securities or other financial instruments are subject to market risk, including partial or total loss of capital. Past performance is not indicative of future results. Always consider your financial situation carefully and consult a licensed financial advisor before making investment or trading decisions.

Engineered for the obsessed. Built for traders.

Purpose-built terminals.

Zero compromise.

Built for speed.

Plot No 1290, 2nd Floor, 17th Cross, 5th Main, Sector-7, HSR Layout, Bangalore 560102

Follow us on

Mintcap Brokers Private Limited

CIN – U66110KA2023PTC178706 | Registered Address: Plot No 1290, Second Floor, 17th Cross, 5th Main, Sector-7, HSR Layout, Bangalore 560102 | Tel: 080 – 49552310 | Email ID: compliance@capmint.com | SEBI registered Stock Broker: INZ000322732 | NSE Cash/F&O Member ID: 90430 | BSE Cash/F&O Member ID: 6903 | MCX Member ID: 57400 | NCDEX Member ID: 1312 | SEBI registered Depository Participant: IN-DP-806-2025 | CDSL DP ID: 12102300 | NSE Clearing Member code: M70108 | AMFI-Registered Mutual Fund Distributor: ARN-289109 (Valid upto 28-Feb-2027) | Category II Execution Only Platform : E6903

Details of Client Bank Account

Compliance Officer: Ms. Shridevi Vungarala | Email ID: compliance@capmint.com | Tel no. + 91 9035330126 | Grievance Redressal Officer (GRO) – Ms. Shikha Gupta | Email ID: Grievance@capmint.com | Tel no: 9035331595.

Procedure to file a complaint on SEBI SCORES: Register on SCORES portal. Mandatory details for filing complaints on SCORES: Name, PAN, Address, Mobile Number, E-mail ID. Benefits: Effective Communication, Speedy redressal of the grievances. You may refer the website https://scores.sebi.gov.in/ for more information. You may also download the SEBI Scores app to log a complaint Android: https://play.google.com > store > apps > sebiscores iOS: https://apps.apple.com > app > sebiscores

Disclaimer

Investment in the securities market are subject to market risks, read all the related documents carefully before investing. Brokerage will not exceed the SEBI prescribed limit.

Mutual fund investments are subject to market risks, read all scheme related documents carefully before investing. Mutual Funds are not exchange-traded products.

Attention Investor:

- Stock Brokers can accept securities as margin from clients only by way of pledge in the depository system w.e.f. September 1, 2020.

- Update your mobile number & email Id with your stock broker/depository participant and receive OTP directly from depository on your email id and/or mobile number to create pledge.

- Pay 20% as upfront margin of the transaction value to trade in cash market segment.

- Investors may please refer to the Exchange’s Frequently Asked Questions (FAQs) issued vide circular reference NSE/INSP/45191 dated July 31, 2020 and NSE/INSP/45534 dated August 31, 2020 and other guidelines issued from time to time in this regard.

- Check your Securities /MF/ Bonds in the consolidated account statement issued by NSDL/CDSL every month.