Table of Content

- Equity Shares vs Preference Shares: At a Glance

- What Are Equity Shares?

- What Do Equity Shares Actually Offer Investors?

- Types of Equity Shares

- What Are Preference Shares?

- What Do Preference Shares Actually Offer Investors?

- Types of Preference Shares

- The Real Difference Between Equity Shares and Preference Shares

- Equity Shares vs Preference Shares: Risk and Return

- Why Do Companies Issue Equity Shares?

- Why Do Companies Issue Preference Shares?

- Similarities Between Equity and Preference Shares

- Equity or Preference Shares: Which One Should You Choose?

- The Mistake Investors Make When Comparing the Two

- Legal and Regulatory Aspects in India

- Frequently Asked Questions

- The Bottom Line

- Read Further

Link copied!

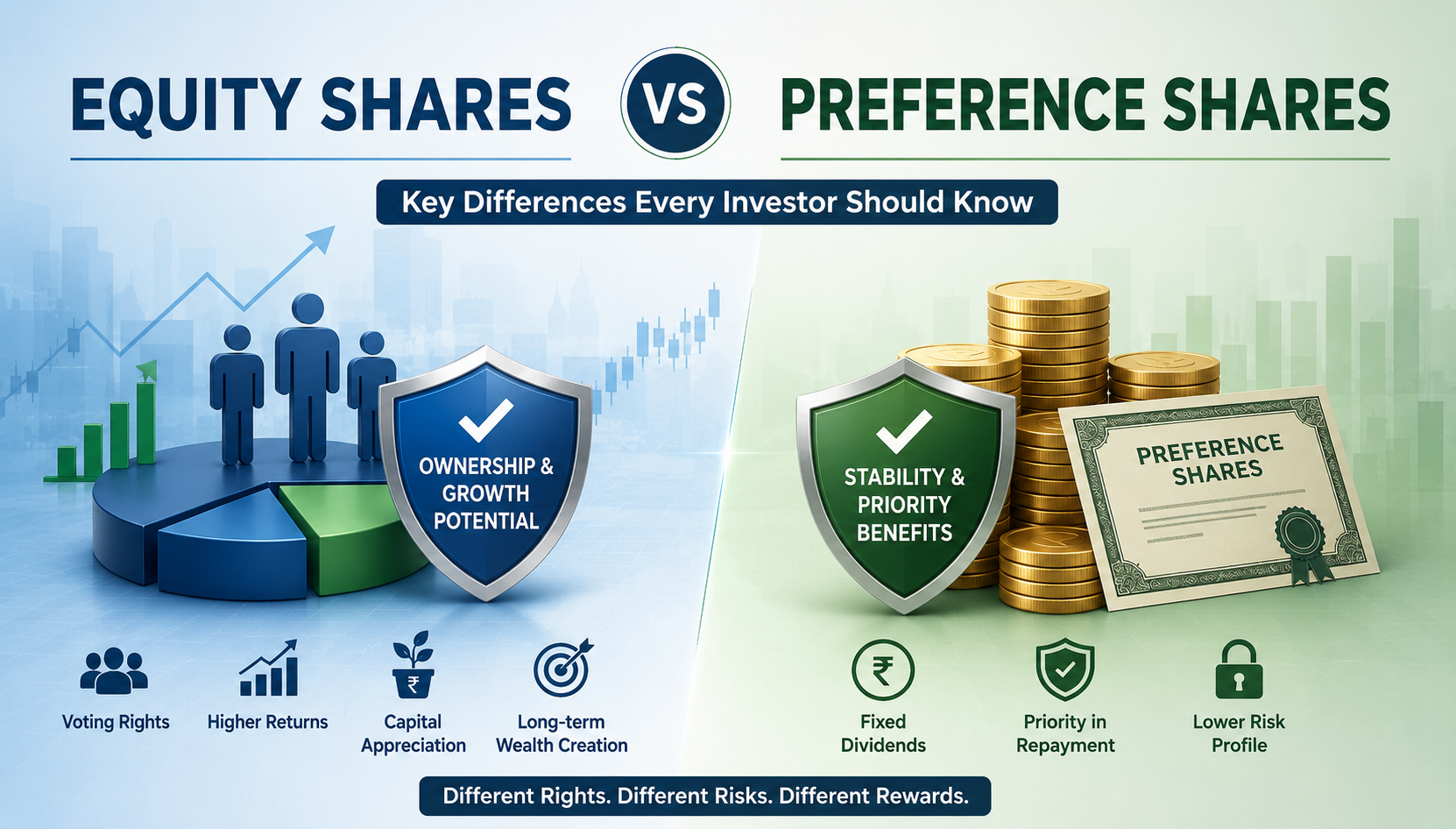

Difference Between Equity and Preference Shares: Which One Fits Your Investment Goals?

Most investors know that buying shares means owning a part of a company.

What they often miss is that not all ownership works the same way.

An equity shareholder participates in the growth of the business, gets voting rights, and takes on the uncertainty that comes with market movements. A preference shareholder stands ahead of equity shareholders when it comes to dividends and repayment of capital, but usually gives up voting rights and much of the upside potential.

So, the difference between preference shares and equity shares is not simply about fixed versus variable dividends. It is about what you want from your investment: growth, income, control, priority, or some combination of these.

Neither type of share is universally better.

The right choice depends on the kind of investor you are.

Equity Shares vs Preference Shares: At a Glance

If you want the quick version, here it is.

|

Basis |

Equity Shares |

Preference Shares |

|---|---|---|

|

Ownership |

Represent ownership in the company |

Represent share capital with preferential rights |

|

Dividend |

Variable and dependent on profits and company decisions |

Generally paid according to predetermined terms |

|

Dividend Priority |

Paid after preference shareholders |

Paid before equity shareholders |

|

Voting Rights |

Generally available |

Usually limited |

|

Capital Repayment |

Paid after creditors and preference shareholders |

Paid before equity shareholders but after creditors |

|

Risk |

Relatively higher |

Generally lower than equity shares |

|

Return Potential |

Higher capital appreciation potential |

More focused on income and capital priority |

|

Redemption |

Generally not redeemable |

May be redeemable according to issue terms |

|

Convertibility |

Generally not convertible |

Certain preference shares can be converted into equity |

|

Suitable For |

Investors seeking long-term growth |

Investors prioritising relatively predictable income |

This table explains the structural difference between equity shares and preference shares.

But it does not answer the more important question: why would an investor choose one over the other?

To understand that, we need to look at what owning each type of share actually means.

What Are Equity Shares?

Equity shares represent ownership in a company.

When you purchase equity shares, you become one of the owners of the business. Your ownership may be extremely small compared with promoters or institutional investors, but the basic principle remains the same: if the company grows, you can participate in that growth.

This is what makes equity investing attractive.

Suppose a company expands its operations, increases profits, gains market share, and becomes more valuable over the next ten years. If the market recognises that growth, the price of its equity shares may increase significantly.

But the relationship works both ways.

If the company performs poorly, loses market share, takes on excessive debt, or faces industry-wide challenges, the value of its equity shares can decline.

Equity shareholders accept this uncertainty in exchange for the possibility of higher long-term returns.

That is the basic bargain of equity ownership.

What Do Equity Shares Actually Offer Investors?

Equity shares are often described using words like ownership, dividends, and voting rights. But these features make more sense when viewed from an investor’s perspective.

Participation in Business Growth

The biggest attraction of equity shares is the opportunity to participate in the long-term growth of a company.

If the business becomes more profitable and valuable, shareholders may benefit through an increase in the market price of their shares.

There is no guaranteed return. But unlike preference shares, the upside is not generally limited to a predetermined dividend rate.

Voting Rights

Equity shareholders generally have the right to vote on important company matters according to their shareholding and applicable laws.

This can include decisions relating to the appointment of directors and other corporate matters placed before shareholders.

For a retail investor with a small holding, this may not translate into significant individual control. But collectively, voting rights make equity shareholders an important part of corporate governance.

Variable Dividends

Equity dividends are not fixed.

A profitable company may decide to distribute part of its earnings to shareholders as dividends. Another company may retain most of its profits to fund expansion.

Even a company that paid dividends in the past may reduce or stop them depending on its financial position and business requirements.

This is why equity investors should never treat dividends as guaranteed income.

Residual Claim on Assets

Here is the part investors often ignore.

If a company is liquidated, equity shareholders stand relatively low in the repayment hierarchy. Creditors and other eligible claimants are paid first, followed by preference shareholders according to their rights. Equity shareholders receive what remains.

Sometimes, very little remains.

This higher risk is one reason equity shareholders expect greater return potential.

Types of Equity Shares

Not all equity shares reach investors in the same way. Companies can issue different forms of equity depending on their objectives.

Ordinary Equity Shares

These are the standard equity shares most investors encounter in the stock market. They generally provide voting rights and the opportunity to receive dividends and benefit from capital appreciation.

Bonus Shares

Bonus shares are additional shares issued to existing shareholders without requiring additional payment.

For example, in a 1:1 bonus issue, an eligible shareholder receives one additional share for every share already held, subject to the terms of the issue.

The number of shares increases, but investors should understand that a bonus issue does not automatically create additional economic value overnight because the share price adjusts to reflect the increased number of shares.

Rights Shares

A rights issue allows existing shareholders to purchase additional shares, generally in proportion to their existing holdings and according to specified terms.

Investors can decide whether participating in the rights issue makes financial sense based on the issue price, company fundamentals, and their investment objectives.

Sweat Equity Shares

Sweat equity shares may be issued to eligible directors or employees in recognition of their contribution, intellectual property, technical expertise, or value addition to the company.

The purpose is different from an ordinary public issue. These shares are generally used to reward people who have contributed directly to building the business.

What Are Preference Shares?

Preference shares sit in an interesting position within a company’s capital structure.

They are shares, but they do not behave exactly like ordinary equity shares.

Preference shareholders receive preferential treatment over equity shareholders in two important areas: the payment of dividends and the repayment of capital during liquidation.

This priority is the defining feature of preference shares.

Suppose a company has both equity and preference shareholders. If dividends are declared according to the applicable terms, preference shareholders receive their dividend entitlement before equity shareholders.

Similarly, if the company is wound up, preference shareholders have priority over equity shareholders when capital is repaid, although creditors and other senior claims still come before shareholders.

This does not make preference shares risk-free.

It simply changes where the investor stands in the capital structure.

What Do Preference Shares Actually Offer Investors?

Preference shares attract a different type of investor.

An equity investor primarily looks at growth potential. A preference shareholder is more concerned with income terms and priority of claims.

Preference in Dividend Payments

Preference shareholders receive dividends before equity shareholders according to the terms attached to the shares.

This creates greater income predictability compared with ordinary equity shares.

But “preference” should not be confused with “guarantee.”

Dividend payments remain subject to the terms of the issue, the financial position of the company, and applicable legal requirements.

Priority During Liquidation

If a company is wound up, preference shareholders stand ahead of equity shareholders for repayment of capital.

But they do not stand ahead of creditors.

This distinction matters.

Preference shares may carry lower risk than equity shares in the repayment hierarchy, but they are still investments in the company and remain exposed to business and financial risk.

Limited Voting Rights

Preference shareholders generally do not enjoy the same voting rights as equity shareholders.

They may, however, receive voting rights in specific circumstances provided under applicable laws, including matters directly affecting their rights.

Redemption and Conversion Features

Depending on the terms of issue, preference shares may be redeemable after a specified period or convertible into equity shares.

These features can significantly change the risk and return characteristics of the investment.

This is why investors should read the actual terms of a preference share issue rather than assuming all preference shares work the same way.

Types of Preference Shares

The term “preference shares” covers several different structures.

Cumulative Preference Shares

If the company does not pay the applicable preference dividend in a particular year, the unpaid amount accumulates and may become payable in future years according to the terms of the shares.

Non-Cumulative Preference Shares

Unpaid dividends generally do not accumulate.

If the applicable dividend is not paid for a particular period, the shareholder usually cannot claim it in subsequent years.

Participating Preference Shares

These shares may allow investors to participate in additional profits or surplus assets beyond their normal preferential entitlement, subject to the terms of issue.

Non-Participating Preference Shares

The investor’s entitlement is generally limited to the preferential benefits specified when the shares are issued.

Convertible Preference Shares

Convertible preference shares can be converted into equity shares according to predetermined terms.

This allows investors to begin with the characteristics of preference shares and potentially participate in equity ownership later.

Non-Convertible Preference Shares

These shares cannot be converted into equity and continue to operate according to their original terms until redemption or another applicable event.

Redeemable Preference Shares

Redeemable preference shares are repaid by the company after a specified period or according to predetermined conditions, subject to applicable company law.

The Real Difference Between Equity Shares and Preference Shares

The equity and preference shares difference becomes clearer when you stop looking only at definitions and start looking at the trade-offs.

Equity shareholders accept greater uncertainty for greater potential upside.

Preference shareholders give up some of that upside and control in exchange for priority.

An equity investor asks:

How much can this business grow?

A preference shareholder is more likely to ask:

What are my dividend terms, where do I stand in the repayment hierarchy, and when can my capital be redeemed?

These are fundamentally different investment questions.

That is why comparing the two solely on the basis of returns can be misleading.

Equity Shares vs Preference Shares: Risk and Return

This is where the difference between equity shares and preference shares matters most to investors.

Equity shares can generate substantial capital appreciation if the underlying company performs well. But they are also directly exposed to changes in business performance, investor sentiment, economic conditions, and stock market volatility.

Preference shares usually offer more predictable return characteristics.

But that predictability comes with a trade-off.

If a company grows rapidly and its equity share price multiplies over several years, preference shareholders may not participate in the same upside unless the shares have conversion or participation features.

So, which is safer?

Preference shares generally stand ahead of equity shares in terms of dividend and capital repayment priority.

But “safer than equity” does not mean “safe.”

The financial health of the company still matters.

Why Do Companies Issue Equity Shares?

Companies need capital to grow.

They may want to build factories, acquire businesses, invest in technology, expand into new markets, reduce debt, or fund long-term projects.

Issuing equity shares allows companies to raise capital without creating the same repayment obligation associated with conventional borrowing.

But equity capital has a cost.

Every time a company issues additional equity shares, the ownership percentage of existing shareholders can be diluted unless they participate proportionately.

Companies, therefore, need to balance the benefits of raising capital against the impact of dilution.

Why Do Companies Issue Preference Shares?

Preference shares give companies another way to structure their capital.

They can attract investors who may not want the uncertainty of ordinary equity but are still willing to invest in the company.

Depending on how they are structured, preference shares can provide flexibility through features such as cumulative dividends, redemption, participation, or conversion into equity.

From the company’s perspective, this creates access to a different pool of capital.

From the investor’s perspective, it creates a different combination of risk and return.

Neither side is getting something for free.

Every additional benefit comes with a trade-off somewhere else in the structure.

Similarities Between Equity and Preference Shares

The differences get most of the attention, but equity and preference shares also have several similarities.

Both form part of a company’s share capital and allow businesses to raise money from investors. Both may provide dividend income, although the terms and priority of payment differ.

Equity and preference shareholders may also have claims on company assets during liquidation, but they stand at different levels in the repayment hierarchy.

Depending on the company and the specific security, both types of shares may also be transferable and available to investors.

The important point is that both represent an investment in the company.

They simply give investors different rights.

Equity or Preference Shares: Which One Should You Choose?

Do not ask which type of share is better.

Ask what you actually want from the investment.

How Much Risk Can You Handle?

If you are comfortable with market fluctuations and short-term uncertainty in exchange for long-term growth potential, equity shares may fit your investment approach.

If you prioritise relatively predictable income terms and priority over equity shareholders, preference shares may be more suitable.

Do You Want Income or Capital Growth?

Equity shares are generally more attractive to investors seeking capital appreciation.

Preference shares are more focused on income and capital priority.

The difference sounds simple, but it changes how you evaluate the investment.

An equity investor studies business growth, earnings potential, competitive advantages, and valuation.

A preference shareholder must pay closer attention to dividend terms, redemption conditions, creditworthiness, and the company’s ability to meet its obligations.

Do Voting Rights Matter to You?

If participation in company decisions matters, equity shares are the more relevant option.

Preference shareholders generally have limited voting rights.

For most small retail investors, voting rights may not be the primary investment consideration. But they remain an important structural distinction between the two types of shares.

What Is Your Investment Horizon?

Equity shares are generally better suited to investors with longer time horizons who can tolerate market cycles.

Preference shares may appeal to investors whose objectives are more focused on income and predetermined investment terms.

But investment horizon should never be considered in isolation.

Liquidity, company fundamentals, valuation, and the specific rights attached to the security matter just as much.

The Mistake Investors Make When Comparing the Two

Many investors assume preference shares are simply “safer equity shares.”

That is an oversimplification.

Preference shares have their own risks.

They may have lower liquidity. Their prices can react to changes in interest rates and the company’s financial condition. The specific terms of redemption, conversion, and dividends can also make one preference share significantly different from another.

Equity shares are easier to understand structurally but harder to predict financially.

Preference shares may appear more predictable financially, but can be more complex structurally.

The lesson is simple.

Do not invest based on the category alone.

Read the terms. Understand the company. Know where you stand in the capital structure.

Legal and Regulatory Aspects in India

In India, equity and preference shares are primarily governed by the Companies Act, 2013, applicable rules, and the company’s Articles of Association. Listed companies are also subject to relevant SEBI regulations and stock exchange requirements.

Equity shareholders generally receive voting rights according to the applicable share structure and legal provisions.

Preference shareholders usually have restricted voting rights but may vote on resolutions directly affecting their rights and in certain other circumstances specified under company law.

The Companies Act also sets conditions relating to the issue and redemption of preference shares. Listed companies face additional disclosure and compliance requirements designed to improve transparency and protect investor interests.

For investors, the regulatory framework matters because the difference between equity and preference shares is not based only on market convention.

Many of these rights and obligations are defined by law and by the specific terms under which the shares are issued.

Frequently Asked Questions

What Is the Difference Between Equity and Preference Shares?

The main difference between equity and preference shares lies in their rights, returns, and repayment priority. Equity shareholders generally receive voting rights and greater capital appreciation potential, while preference shareholders receive priority in dividend payments and repayment of capital over equity shareholders.

What Are Preference Shares?

Preference shares are shares that provide investors with preferential rights over equity shareholders, particularly regarding dividend payments and repayment of capital during liquidation. They generally carry limited voting rights.

What Is Meant by Equity Shares?

Equity shares represent ownership in a company. Investors holding equity shares may receive voting rights, dividends, and the opportunity to benefit from an increase in the company’s share price.

Are Preference Shares Equity?

Preference shares form part of a company’s share capital but have characteristics associated with both equity and fixed-income securities. They provide preferential rights over ordinary equity shareholders but generally offer limited voting rights and different return characteristics.

Which Is Better: Equity Shares or Preference Shares?

Neither is universally better. Equity shares may suit investors seeking long-term growth and willing to accept higher market risk. Preference shares may appeal to investors who prioritise relatively predictable income and preferential claims over equity shareholders.

Are Preference Shares Safer Than Equity Shares?

Preference shares generally have priority over equity shares for dividend payments and repayment of capital. However, they are not risk-free. Investors remain exposed to the financial health of the issuing company, liquidity risk, and the specific terms of the shares.

Can Preference Shares Be Converted Into Equity Shares?

Yes, convertible preference shares can be converted into equity shares according to predetermined terms and conditions. Non-convertible preference shares do not provide this option.

Do Preference Shareholders Have Voting Rights?

Preference shareholders generally have limited voting rights. However, they may vote on matters directly affecting their rights and in other circumstances specified under applicable company law.

The Bottom Line

The difference between preference shares and equity shares is ultimately a difference in what the investor is willing to exchange.

Equity shareholders accept uncertainty for growth potential and ownership rights.

Preference shareholders give up some control and potential upside for priority in dividends and capital repayment.

Neither choice is automatically better.

The investor chasing growth may find preference shares too restrictive. The investor looking for relatively predictable income may find equity volatility unnecessary.

The company does not care which category sounds more sophisticated.

The market does not reward you for choosing the instrument with the highest theoretical return.

What matters is whether the security fits your financial objective, your risk tolerance, and the role you expect it to play in your portfolio.

Most investment mistakes begin when people buy first and understand the instrument later.

Reverse that order.

Know what you own. Know what rights come with it. And know exactly what you are giving up in exchange.

Read Further

Disclaimer: This content is for educational purposes only and does not constitute financial or investment advice. Investments in securities or other financial instruments are subject to market risk, including partial or total loss of capital. Past performance is not indicative of future results. Always consider your financial situation carefully and consult a licensed financial advisor before making investment or trading decisions.

Table of Content

- Equity Shares vs Preference Shares: At a Glance

- What Are Equity Shares?

- What Do Equity Shares Actually Offer Investors?

- Types of Equity Shares

- What Are Preference Shares?

- What Do Preference Shares Actually Offer Investors?

- Types of Preference Shares

- The Real Difference Between Equity Shares and Preference Shares

- Equity Shares vs Preference Shares: Risk and Return

- Why Do Companies Issue Equity Shares?

- Why Do Companies Issue Preference Shares?

- Similarities Between Equity and Preference Shares

- Equity or Preference Shares: Which One Should You Choose?

- The Mistake Investors Make When Comparing the Two

- Legal and Regulatory Aspects in India

- Frequently Asked Questions

- The Bottom Line

- Read Further

Engineered for the obsessed. Built for traders.

Purpose-built terminals.

Zero compromise.

Built for speed.

Plot No 1290, 2nd Floor, 17th Cross, 5th Main, Sector-7, HSR Layout, Bangalore 560102

Follow us on

Mintcap Brokers Private Limited

CIN – U66110KA2023PTC178706 | Registered Address: Plot No 1290, Second Floor, 17th Cross, 5th Main, Sector-7, HSR Layout, Bangalore 560102 | Tel: 080 – 49552310 | Email ID: compliance@capmint.com | SEBI registered Stock Broker: INZ000322732 | NSE Cash/F&O Member ID: 90430 | BSE Cash/F&O Member ID: 6903 | MCX Member ID: 57400 | NCDEX Member ID: 1312 | SEBI registered Depository Participant: IN-DP-806-2025 | CDSL DP ID: 12102300 | NSE Clearing Member code: M70108 | AMFI-Registered Mutual Fund Distributor: ARN-289109 (Valid upto 28-Feb-2027) | Category II Execution Only Platform : E6903

Details of Client Bank Account

Compliance Officer: Ms. Shridevi Vungarala | Email ID: compliance@capmint.com | Tel no. + 91 9035330126 | Grievance Redressal Officer (GRO) – Ms. Shikha Gupta | Email ID: Grievance@capmint.com | Tel no: 9035331595.

Procedure to file a complaint on SEBI SCORES: Register on SCORES portal. Mandatory details for filing complaints on SCORES: Name, PAN, Address, Mobile Number, E-mail ID. Benefits: Effective Communication, Speedy redressal of the grievances. You may refer the website https://scores.sebi.gov.in/ for more information. You may also download the SEBI Scores app to log a complaint Android: https://play.google.com > store > apps > sebiscores iOS: https://apps.apple.com > app > sebiscores

Disclaimer

Investment in the securities market are subject to market risks, read all the related documents carefully before investing. Brokerage will not exceed the SEBI prescribed limit.

Mutual fund investments are subject to market risks, read all scheme related documents carefully before investing. Mutual Funds are not exchange-traded products.

Attention Investor:

- Stock Brokers can accept securities as margin from clients only by way of pledge in the depository system w.e.f. September 1, 2020.

- Update your mobile number & email Id with your stock broker/depository participant and receive OTP directly from depository on your email id and/or mobile number to create pledge.

- Pay 20% as upfront margin of the transaction value to trade in cash market segment.

- Investors may please refer to the Exchange’s Frequently Asked Questions (FAQs) issued vide circular reference NSE/INSP/45191 dated July 31, 2020 and NSE/INSP/45534 dated August 31, 2020 and other guidelines issued from time to time in this regard.

- Check your Securities /MF/ Bonds in the consolidated account statement issued by NSDL/CDSL every month.